Amazon - The $200 Billion Misunderstanding

The market sees Amazon setting cash on fire. I see the most formidable moat in the history of markets.

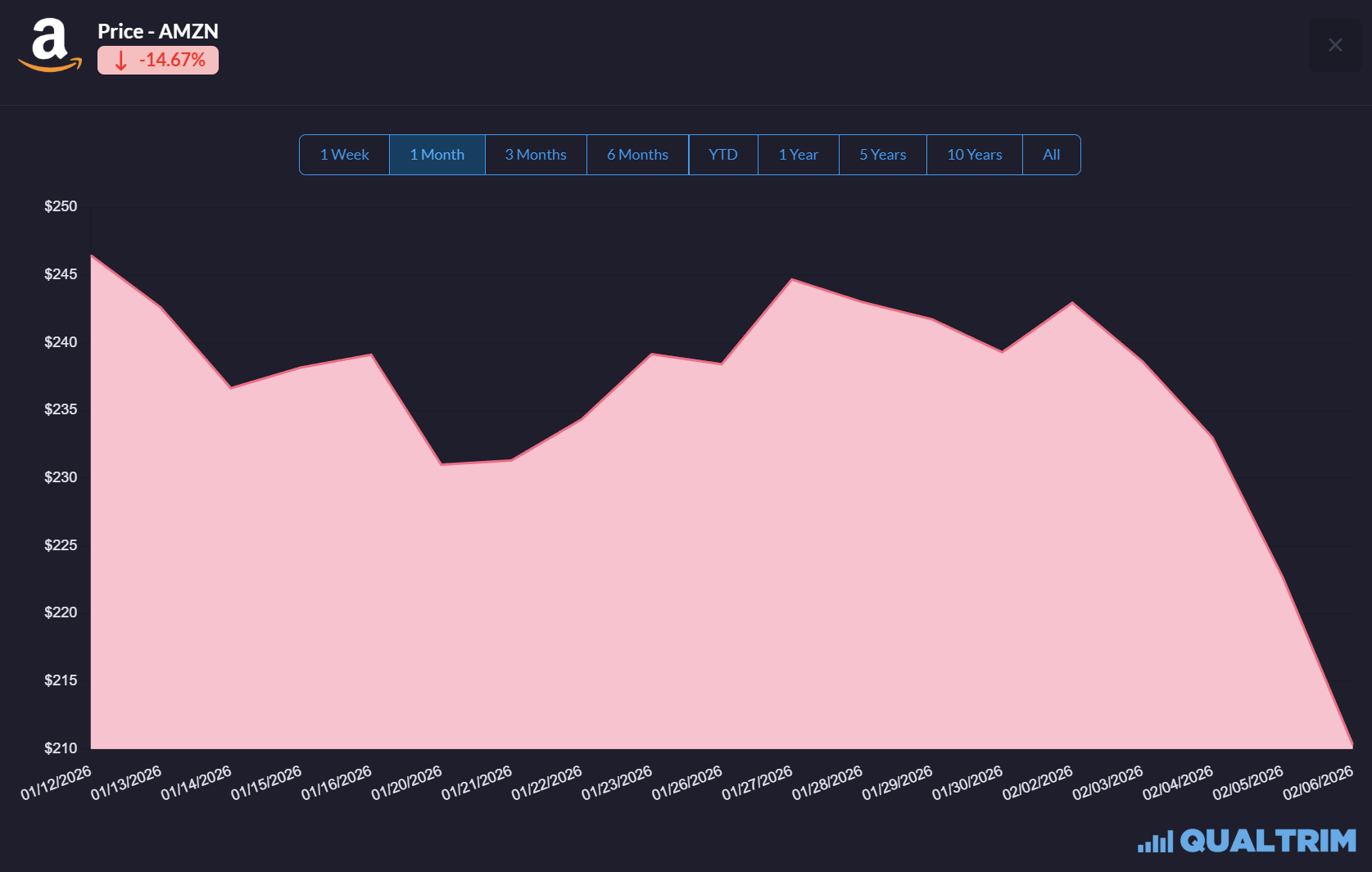

The market’s reaction to Amazon’s Q4 earnings report was violent and, in my opinion, wrong.

Shares are now down nearly 15% in the last month, dragging the broader technology sector down with them.

The narrative forming is one of out of control spending and profit misses.

They see a company setting cash on fire. I see a company building the most formidable moat in the history of free markets.

Market Panic

Let us begin by establishing exactly what happened on Thursday evening to cause such concern.

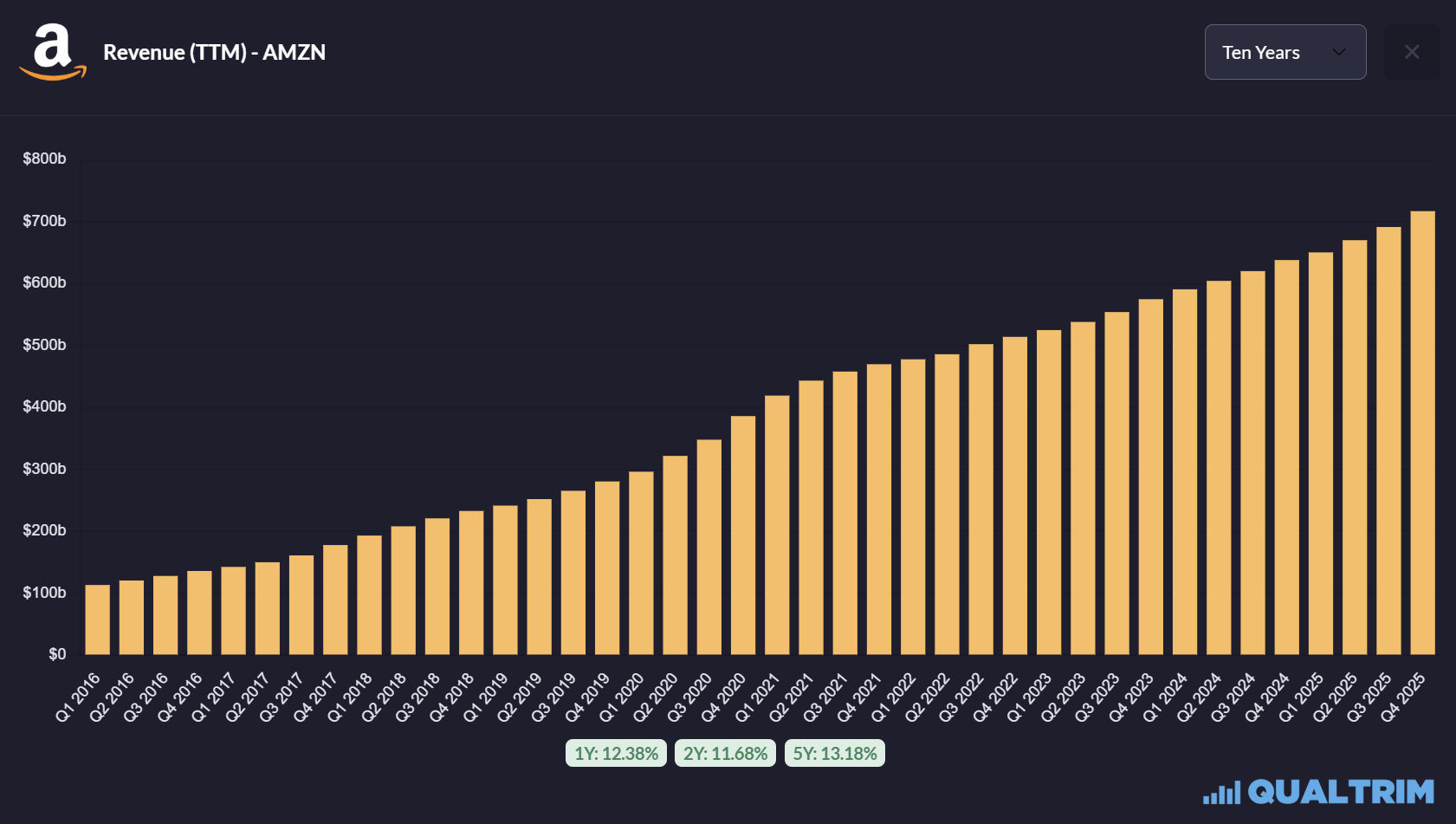

Amazon reported Q4 revenue of $213.4 billion.

$213.4 billion.

In 90 days, this company generated revenue that exceeds the GDP of New Zealand.

That number represents nearly 14% YoY growth, comfortably beating the consensus estimate of roughly $211 billion. For a company of this size to be accelerating revenue growth back into the mid teens is a remarkable feat of execution.

The market, however, did not care about the revenue beat. It fixated on two numbers.

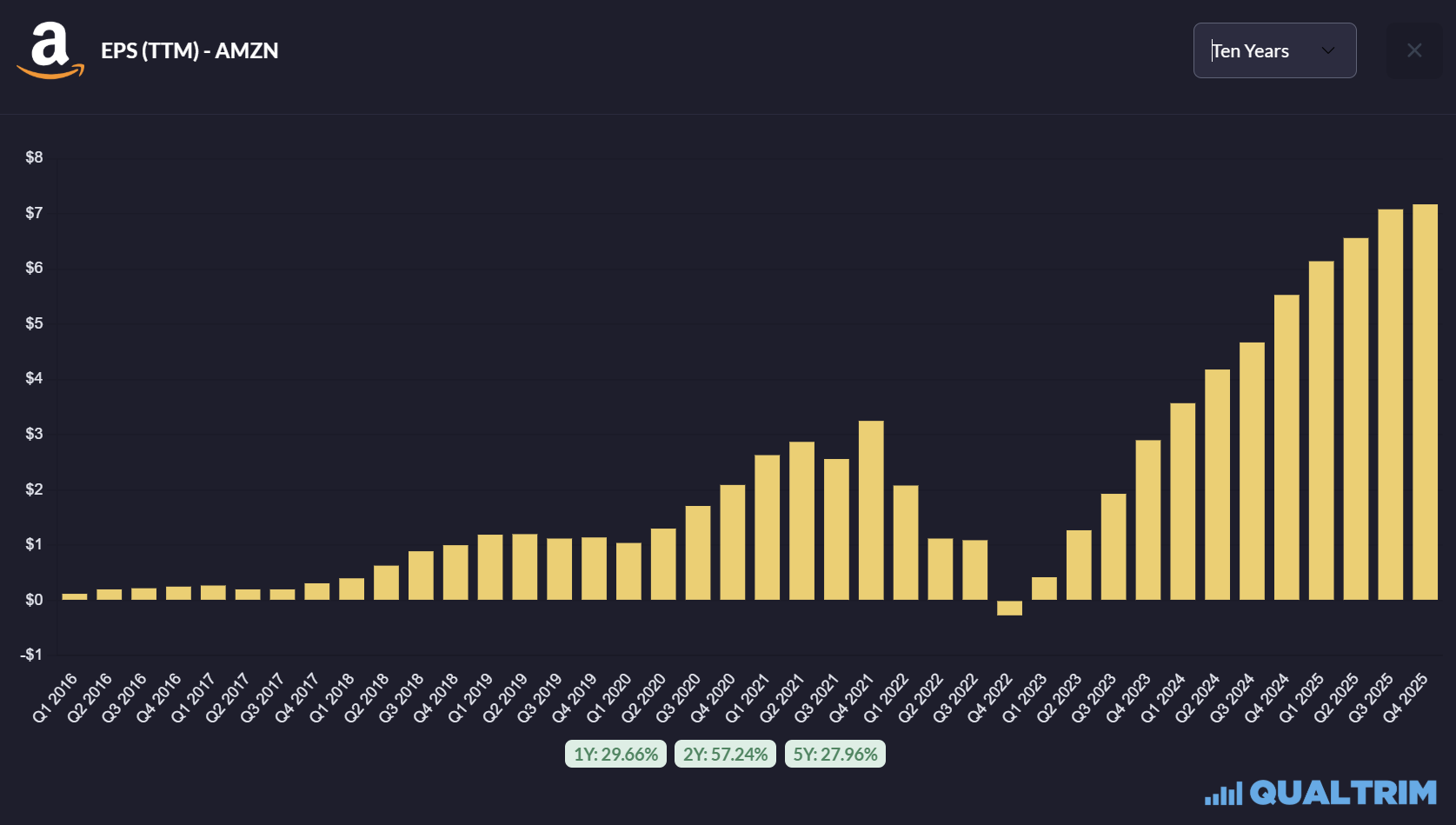

The first was EPS. Amazon reported $1.95, missing the analyst consensus of $1.97 by $0.02.

It seems in today’s world, a miss is a miss.

Any human being capable of reading can see that this miss was artificial. It was caused by accounting noise created by three different one-off charges.

There was a $1.1 billion charge for the resolution of tax disputes, primarily in Italy. There was a $730 million charge for severance costs associated with the Project Dawn restructuring. And there was a $610 million charge for asset impairments related to the closure of physical stores.

These are non recurring items. Unless you believe Amazon plans to settle a billion dollar tax dispute every single quarter for the rest of eternity, you should strip these out.

If you do so, the adjusted operating income was not $25 billion but over $27.4 billion.

That is not a miss. That is a massive beat.

The underlying profitability of the business is stronger than it has ever been.

But the real source of the panic was not the past. It was the future. Management guided to CapEx of ~$200 billion for 2026. This is up from $125 billion in 2025. It is a number so large it is difficult to comprehend.

To put it in context, Amazon plans to spend more on infrastructure in one year than the entire market cap of Intel or Boeing. The market looked at this number, looked at the resulting decline in FCF, and hit the sell button.

They interpreted it as reckless spending.

This interpretation is flawed. It ignores the history of this company and the nature of the technological revolution we are living through.

Andy Jassy is not spending $200 billion on vanity projects. He is not building a metaverse that nobody wants to visit.

He is building the physical infrastructure of the future.

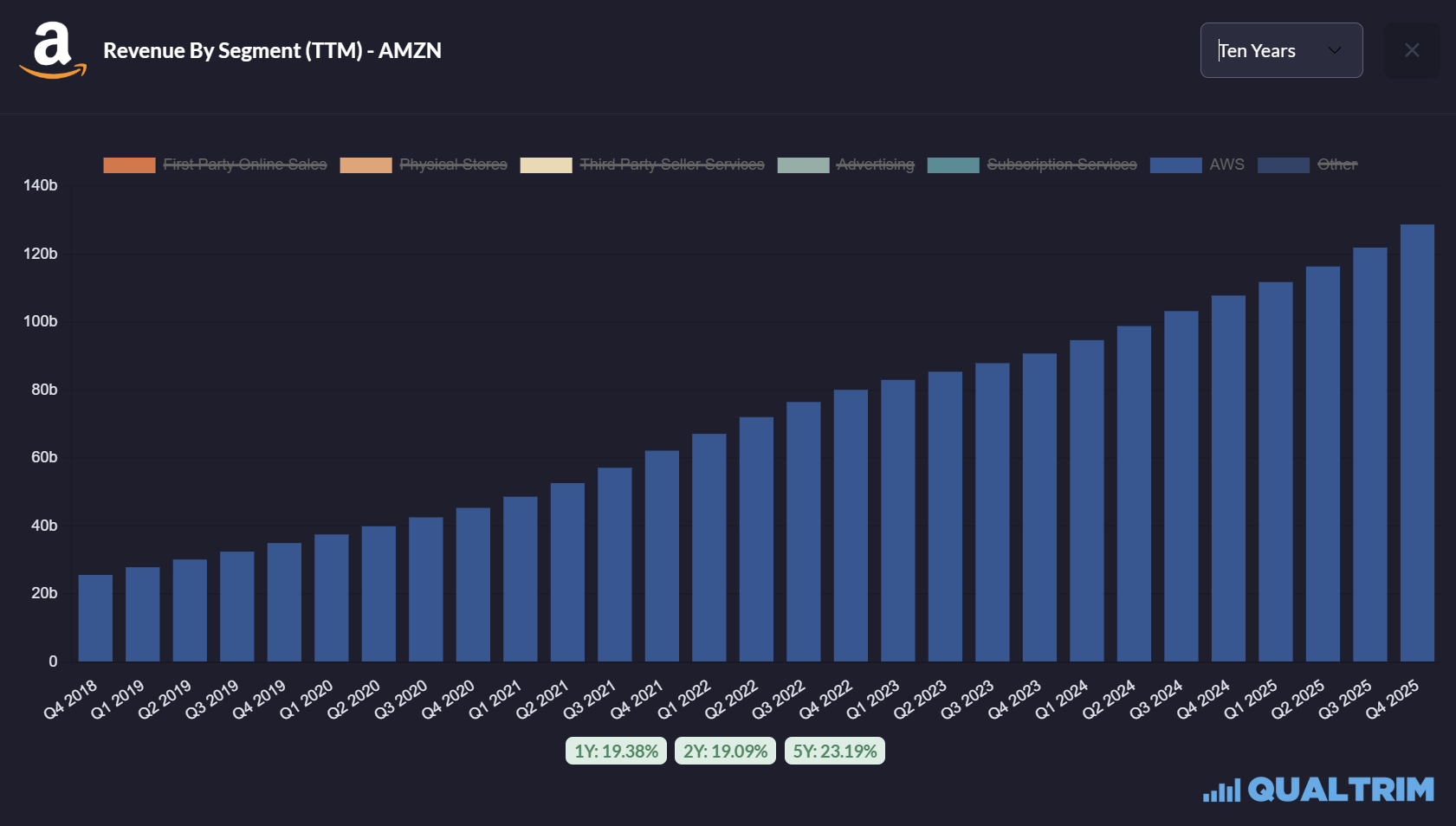

AWS

To understand why this spending is necessary, you have to look at AWS. For the last two years, the bear case on Amazon was that Microsoft Azure was stealing market share.

The narrative was that Microsoft’s partnership with OpenAI gave it an insurmountable lead in AI and that AWS would be relegated to legacy workloads.

The Q4 results shattered that narrative.

AWS revenue grew by 24% YoY to $35.6 billion.

This is the fastest growth rate the division has posted in 13 quarters. It is an acceleration from the 20% growth seen in Q3 and the 12% growth seen in 2023.

When a business operating at a $142 billion annual revenue run rate accelerates its growth by 4 percentage points, something structural has changed.

That change is the transition of GenAI from experimentation to production.

Throughout 2024 and 2025, enterprises were running pilots. They were testing chatbots in sandboxes. Now they are deploying agents and large scale inference models into production.

And they are choosing to run them on AWS.

The backlog for AWS now stands at $244 billion, up 40% YoY. This is contractually committed future revenue.

The problem Amazon faces is not a lack of demand. It is a lack of capacity.

They physically cannot build data centres fast enough to meet the orders they already have. When you have customers begging to give you money and your only constraint is your ability to provision servers, you do not hoard cash. You build capacity. You spend every dollar you can to capture that market share because in the cloud business, scale is the only moat that matters.

This $200 billion capex bill is not a bet on an uncertain future. It is a necessity.

If Amazon tries to optimise for FCF in 2026, they will lose market share.

They will cede the future to Microsoft and Google. By spending now, they are securing their dominance for the next decade.

Read the rest of this analysis to unlock:

The Silicon Alpha - Why Amazon’s custom chip strategy, Trainium, is a hidden $10B+ business that captures Nvidia’s margins.

The Cash Cow - How the advertising segment has become larger than the entire global newspaper industry.

The Price Target - My SOTP and DCF analysis, revealing a fair value significantly higher than the current trading price.

Subscribe now to see why the market is wrong and access the full valuation model.