Bloom Energy - Solving the Data Centre Crisis

Forget Chips, Buy Power: Why Bloom Energy (BE) is the Ultimate AI Infrastructure Play

I made this call at the start of the year because I had never seen a more bullish confluence of events for any given sector at any given time all throughout my investing career.

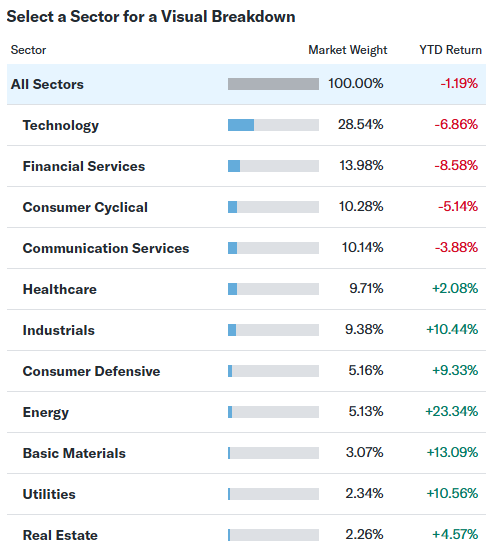

Fast forward to March, and this has aged exceptionally well, with energy massively outperforming all other sectors YTD.

The trends that caused this outperformance are still very much intact, and I think we are still early today. I expect energy outperformance to continue over the next decade, and likely further.

Welcome to the third edition in my mini-series on the companies benefitting most from the energy grid constraints in the USA.

The current state of the Middle East makes these companies even more important than they already were, and I am growing more and more bullish on specifically grid operators and nuclear energy producers as time goes on.

In parts 1 and 2 of the mini-series, I covered GEV and ETN. Today I will cover BE.

Bloom Energy, or BE, is currently trading around $145/share.

Over the last year, this equity has risen dramatically from the ashes of the alternative energy bear market.

These explosive returns were driven by a sudden and violent realisation from the world’s largest technology companies. The realisation is incredibly simple.

It is physically impossible to run a gigawatt-scale AI data centre without electricity, and the legacy utility grid is entirely incapable of providing it.

The market is currently presenting a compelling entry point into a business that has successfully commercialised solid oxide fuel cell technology, sits on a $20 billion total backlog, and operates with a time-to-power advantage that neither gas turbines nor small modular nuclear reactors can currently match.

The narrative driving the recent financial coverage of this sector is a cocktail of awe and panic regarding energy consumption. A slight misunderstanding of supply chain risks regarding critical minerals, the complexity of valuing pre-profit hardware manufacturers transitioning to profitability, and a sudden panic about grid capacity have created a highly volatile trading environment.

However, looking past the daily price action reveals a company that is fundamentally reshaping how hyperscalers procure electricity.

There is a 35-gigawatt energy gap emerging by 2030.

The integration of proprietary solid oxide fuel cells directly on-site at data centres provides a moat that traditional utility providers cannot easily breach. The market is currently pricing BE as a cyclical hardware business, discounting the massive recurring service revenue embedded within its commercial agreements.

The Core Problem

The modern electrical grid was designed for a post-war industrial economy.

It was built to support predictable and slow-growing domestic and commercial loads.

It was absolutely not designed to support 50,000-acre data centre campuses demanding two gigawatts of constant power.

The AI industry is currently undergoing a structural transition. In the early days of LLMs, the primary focus was on training. Training workloads involve feeding massive datasets into clusters of GPUs over several months.

These training facilities could be located anywhere in the world, preferably where land and electricity were cheap, because latency was not a primary concern. However, the industry has now entered the inference era.

Inference is the actual application of the model when a user asks a question or an autonomous system requests a calculation. Inference requires incredibly low latency.

It is impossible to serve real-time financial data or autonomous driving commands from a server located three thousand miles away.

Therefore, inference data centres must be built near major population and financial centres. The problem is that these locations already suffer from heavily congested electrical grids.

In regions like Northern Virginia, which remains the largest data centre market in the world, the power capacity is effectively exhausted. Utilities are currently informing hyperscalers that new grid connections for large loads will take anywhere from three to seven years to complete.

The US currently has around 25 gigawatts of data centre capacity. Over the next five years, an additional 55 gigawatts of capacity is expected to enter the development pipeline.

The grid simply cannot absorb this demand at this pace. A single gigawatt of power is roughly equivalent to the output of a traditional nuclear reactor. Attempting to draw this much power from existing regional substations can trigger cascading blackouts.

In July 2024, a voltage fluctuation in Northern Virginia triggered the simultaneous disconnection of 60 data centres, prompting a massive power surplus that forced emergency adjustments to prevent grid failure.

When a tech company is spending billions of dollars on highly advanced semiconductors, they cannot afford to let those chips sit idle while waiting half a decade for a utility company to build a high-voltage transmission line.

Time-to-power is the single most critical metric in the AI arms race. The cost of capital tied up in idle servers completely destroys the ROI for these facilities. This is the exact friction point where BE extracts its value.

Data centre operators are taking responsibility for their own power needs, with projections indicating that 30% of all sites will use onsite power as their primary energy source by 2030.

Solid Oxide Fuel Cells

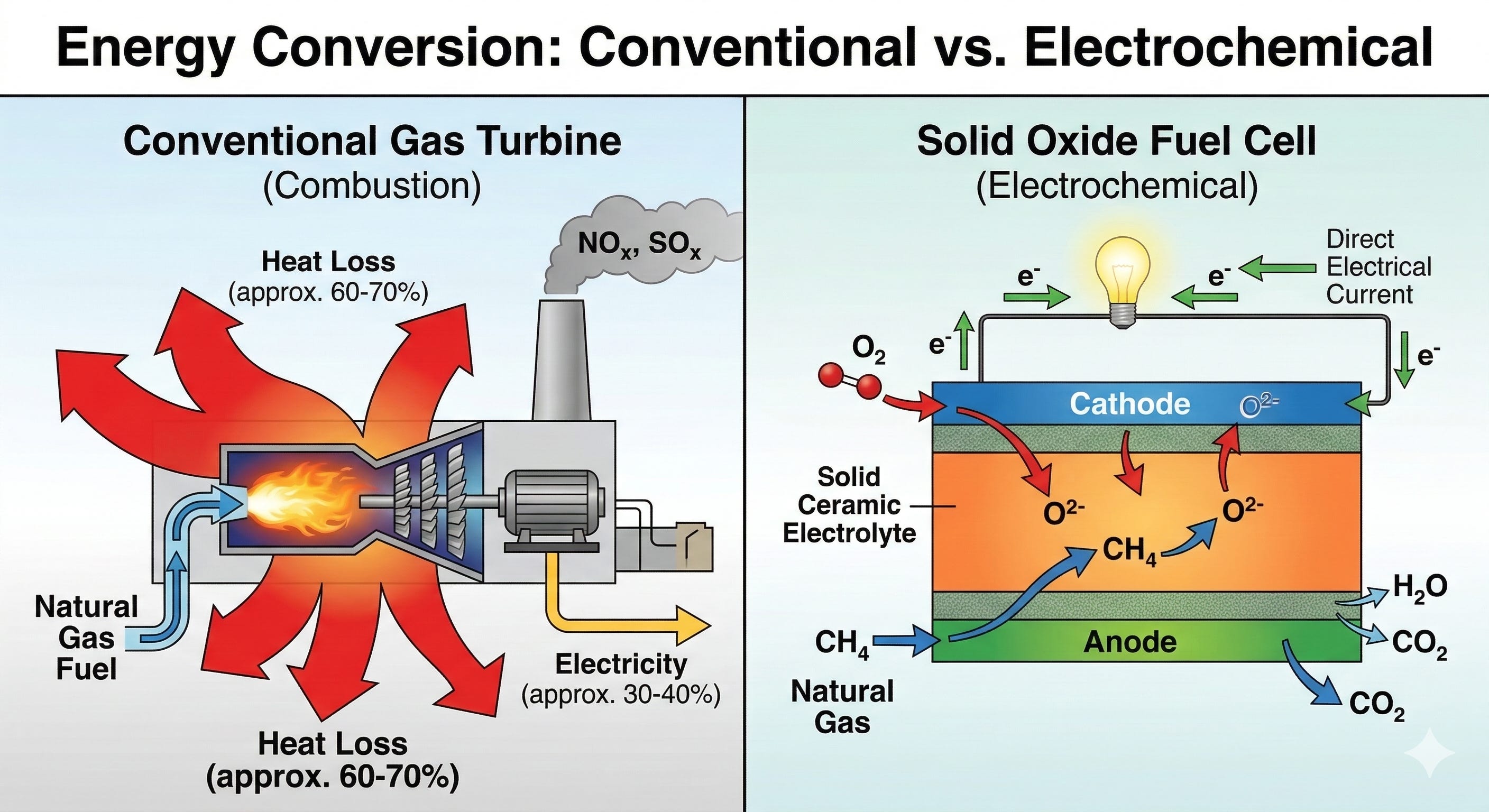

The company’s solid oxide fuel cell technology is its economic moat.

A traditional gas turbine burns natural gas to spin a generator. This combustion process is inherently inefficient, typically converting only 30-40% of the fuel energy into electricity, while the rest is lost as heat.

Furthermore, combustion produces nitrogen oxides and sulphur oxides, which creates massive permitting issues with local environmental protection agencies. Securing an air quality permit for a large gas turbine in a populated area can take years.

BE solid oxide fuel cells operate on an entirely different principle.

They convert fuel directly into electricity through an electrochemical process without any combustion. The fuel cell is simply a solid ceramic electrolyte. When heated to high temperatures, oxygen ions migrate through the crystal lattice of the electrolyte.

They react with a fuel source, such as natural gas or biogas, on the anode side of the cell. This reaction releases electrons, creating a direct electrical current.

Because there is no burning, there are virtually no nitrogen oxide or sulphur oxide emissions.

The electrical efficiency of a Bloom fuel cell is roughly 60%, which is dramatically higher than a standard gas turbine.

If the data centre operator captures the exhaust heat and routes it through an absorption chiller to provide cooling for the servers, the overall system efficiency becomes staggering, cutting data centre electricity use by at least 20%.

The physical footprint of the technology provides another massive advantage. Data centre real estate is incredibly expensive, and local communities frequently oppose the visual blight of massive industrial power plants.

Traditional gas turbines or backup diesel generators require massive amounts of space. Gas turbines typically provide around 50 megawatts of power per acre. Bloom Energy has engineered its fuel cells into a modular, stacked configuration.

By stacking the units four-high, BE can deliver 100 megawatts of power within a single acre. This footprint density is completely unmatched in the onsite power generation industry.

Most importantly, the modular nature of the technology provides extreme reliability.

A BE server is composed of dozens of independent 65-kilowatt modules. If one module fails or requires maintenance, it can be swapped out without shutting down the entire system.

This completely eliminates the risk of a single point of failure causing a total site outage. As a result, BE offers four nines of availability, ensuring the 99.99% uptime that data centres demand.

AI workloads are highly volatile. When a cluster of processors begins a complex calculation, the power draw spikes instantaneously. Traditional grid infrastructure struggles to respond to these microsecond oscillations.

BE solves this by integrating ultra-capacitors into their systems. These capacitors act as an instantaneous discharge and recharge buffer, absorbing the massive spikes and troughs of the computing workload before they can destabilise the primary power generation unit.

The defining advantage is deployment speed.

While a utility connection takes years, and a gas turbine takes up to three years from order to delivery, BE can deploy its fuel cells in a fraction of the time. In some urgent cases, such as their deployment for Oracle Cloud Infrastructure, Bloom successfully delivered onsite power within 55 days of the initial 90-day delivery request.

This ability to bypass the utility interconnection queue entirely is the primary reason hyperscalers are willing to sign multi-billion dollar procurement contracts.

Landmark Commercial Agreements

The narrative surrounding BE shifted dramatically between the end of 2024 and the beginning of 2026. The company moved from being viewed as a provider of niche secondary backup power to becoming the primary baseload power plant for global AI factories.

This transition was cemented by two massive commercial agreements that altered the entire trajectory of the business.

The first was the $5 billion partnership with Brookfield Asset Management, announced in October 2025. Brookfield is one of the largest infrastructure investors on the planet, possessing immense capital and global real estate capabilities.

They did not simply buy equipment from Bloom Energy. They formed a partnership to co-develop integrated facilities worldwide, where Bloom solid oxide fuel cells serve as the primary power plant, completely independent of the local grid.

This deal was a clear validation from institutional capital that fuel cells are now a bankable, tier-one infrastructure asset class. The arrangement covers the design, construction, and long-term power delivery for multiple AI campuses, beginning with sites in Europe.

The second major catalyst was the $2.65 billion agreement with American Electric Power, which was finalised in January 2026. This deal is particularly fascinating because American Electric Power is a traditional utility company.

Utilities usually build transmission wires and substations. The fact that a utility is purchasing up to 1 gigawatt of behind-the-meter fuel cells demonstrates how broken the traditional grid expansion model has become.

This specific deployment is aimed at supporting the Cheyenne AI Factory in Wyoming, a massive 1.8-gigawatt campus developed by Crusoe and Tallgrass. The first phase of this project relies entirely on 900 megawatts of Bloom Energy fuel cells, specifically chosen because the technology can entirely bypass the regional interconnection queue.

This deployment includes a 20-year offtake agreement with a high-grade customer, providing Bloom Energy with absolute revenue certainty. Analysts estimate that this single Wyoming deployment will generate $3 billion in revenue for Bloom over its lifespan.

Data centre operators are no longer treating onsite generation as a temporary bridge until the utility arrives. Onsite power is now the permanent, primary energy strategy for the these companies.

By the end of this decade, 30% of all data centre sites will rely on onsite power as their primary energy source. BE is perfectly positioned to capture the majority of this structural shift.

We have established the macro necessity of Bloom’s technology and the unprecedented backlog of energy demand. However, the real alpha lies in how efficiently management can translate this narrative into cash flow, and how the market is currently mispricing that transition.

🔒 What’s Inside for Premium Subscribers:

The Financial Inflection Point - A deep dive into the Q4 2025 earnings, the shock 58% revenue growth guidance for 2026, and proof that the cash burn era is over.

The $20 Billion Backlog Floor - Unpacking Bloom’s 100% service attach rate and why the market is entirely undervaluing its 20% margin recurring revenue.

The Competitor Reality Check - Why the retail market’s current obsession with theoretical nuclear startups and bottlenecked legacy giants is creating a massive mispricing opportunity in BE today.

The Supply Chain Threat - The geopolitical risks regarding rare earths and pipeline limits that could break the thesis.

My Full DCF Valuation - Step-by-step access to my base-case model, including my precise price target and why the stock still has room to run despite recent rallies.

To unlock the full DCF model, competitive teardown, and risk analysis for Bloom Energy, upgrade your subscription below.