Disclaimer: This is in no way financial advice. I am not a financial advisor. Do your own research before making any final decision on investments.

Who are Domino’s Pizza (Ticker: DPZ)?

Domino’s Pizza ranks amongst the biggest pizza chains worldwide, known for quick delivery and consistent but delicious food. Over the years, they’ve built a well-recognized name by embracing online ordering, speeding up service, and maintaining their great product quality.

Domino’s is well diversified, operating in more than 90 countries. Since it’s a go-to choice for many pizza fans, the brand has strong staying power in a competitive market.

They were quick to jump on digital ordering through their user-friendly website and mobile app, which has given them a solid advantage. Extras like the “Pizza Tracker” let customers see where their order is at every step, building trust and loyalty. The company also uses data insights to boost delivery routes and manage inventories, saving time and money.

The company franchises most of their locations, which I like since they can simply collect fees and royalties rather than handling day-to-day operations for every store (a strategy McDonalds also uses). They also manage a good part of their own supply flow, which helps franchisees lock in steady ingredient costs. This approach keeps product quality consistent and can improve local store profits.

How are They Doing Financially?

According to the most recent 10-K report, Cash from Operations was up 24.3% YoY to $591 million. Capital expenditures was $105 million, meaning their annual Free Cash Flow (FCF) was an impressive $486 Million.

The concern for DPZ is that their Cash and Cash Equivalents at the end of 2023 was just $114 million. The reality is that most of the cash they have is not currently available and is noted on their 10-K as restricted. This means they’re holding it for specific purposes like interest payments or advertising and therefore, it is not available for general use.

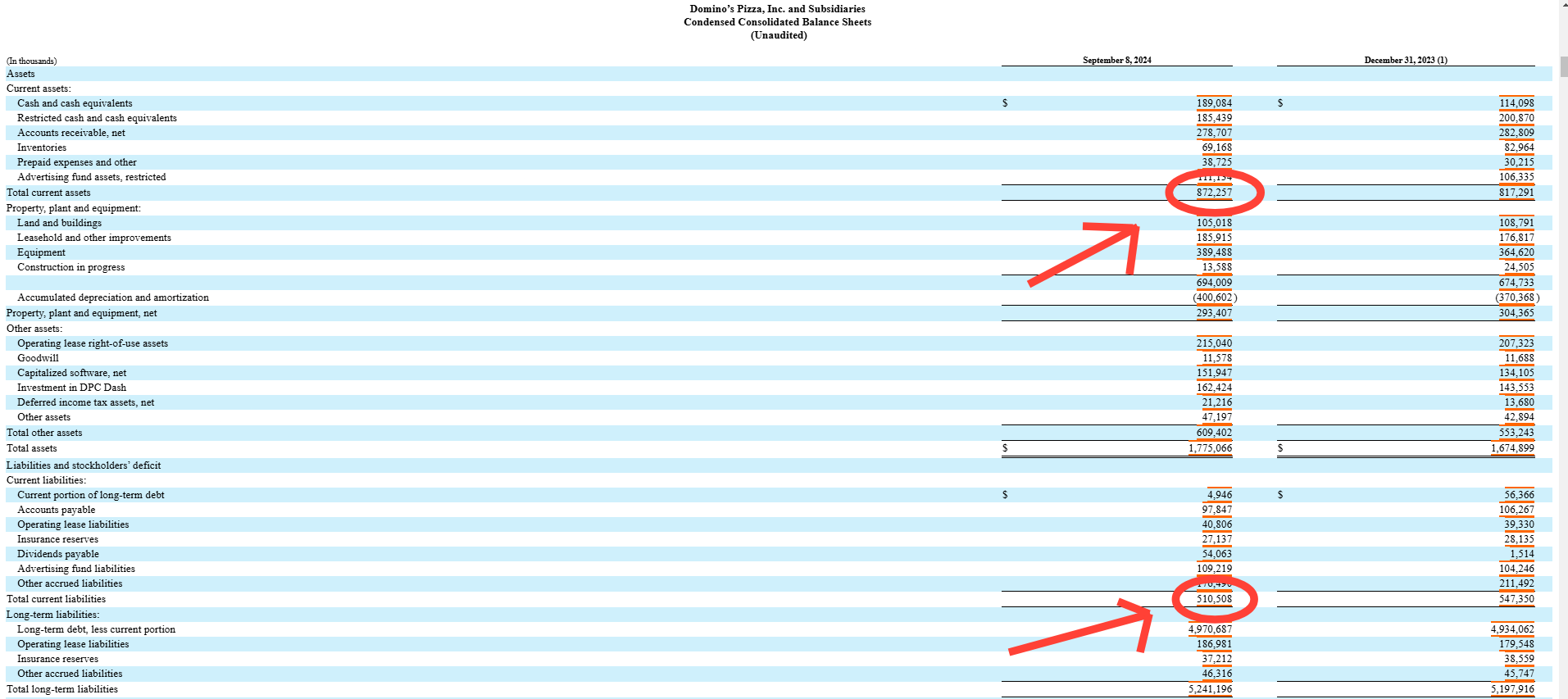

This raises concerns over their short term liquidity, so let’s take a look at their latest 10-Q report:

Current Assets are $872 Million and Current Liabilities are $510 Million

Domino's is therefore in a very healthy position to meet its short-term obligations, and given the high-quality earnings and strong annual Free Cash Flow, Domino’s looks to be a very high quality company in a strong position financially.

Why is the Price Down So Much?

DPZ is down around 22% from it’s peak in late 2021, and down 19% from it’s highs in 2024. When the pandemic hit, Domino’s thrived because the average person stuck at home obviously ordered much more delivery than usual. This fuelled rapid sales gains and sent the stock to impressive highs.

Once lockdowns eased and dining habits shifted again, growth cooled off. At the same time, stiff competition from other delivery platforms ramped up, and higher costs for labour and ingredients has squeezed DPZ’s margins over the last couple of years.

The stock dropped again in 2024, with management suspending guidance of international store growth a largely contributing factor. However they did maintain their long-term sales and income growth guidance, meaning this dip could be viewed as an attractive entry point.

What are the Risks?

DPZ has an enormous amount of Long-Term debt. Looking at the balance sheet their Total Assets are $1.78 Billion and their Total Liabilities are $5.20 Billion. This gives them a Debt to Assets ratio of 2.93! The main question for this company becomes how on earth are they going to manage this massive Long-Term debt?

To answer this we can look to the company’s Interest Coverage Ratio. The company’s annual EBIT (Earnings Before Interest and Taxes) was $849 Million as of their most recent report. Compare this to the annual Interest Expense of $185 Million and you get an Interest Coverage Ratio of 4.59. This means they generate $4.59$ for every $1.00$ they pay in interest.

This is very reassuring, and proves a deeper look into a company’s balance sheet can certainly reveal more than what first meets the eye.

Domino’s has staggered maturities on its bonds and loans, reducing the risk of a severe near-term liquidity crunch. However, the rise in interest rates post 2022 will increase refinancing costs when outstanding debt matures. Management’s approach to refinancing - especially if rates stay elevated (which I think they most likely will in 2025) - remains an important watch-point during future earnings reports.

Is Domino’s Pizza Undervalued?

To show you how fast this company is compounding I want to perform Bogle’s Valuation. This simply shows the stock’s expected future return. To do this we apply the formula:

Expected Return = Earnings Growth + Shareholder Yield + Multiple Expansion

Earnings growth is forecast by DPZ management to be about 7.5% over the next 4 years as shown from their 2024 Q3 Earnings Release

Shareholder Yield is Dividend Yield + Buyback Yield (I will use the average from the last 5 years), which is 1.5% + 3.5% = 5% Shareholder Yield which is enormous considering how fast this company is growing.

Multiple expansion will most likely be negative, the current forward P/E ratio of 25 is very high for a Consumer Discretionary company, so if we can assume this will decrease at moderate 2% per year on average.

Earnings Growth (7.5%) + Shareholder Yield (5%) + Multiple Expansion (-2%) gives us an Expected Annual Return of 10.5% . This is obviously enormous, and with this in mind I think the company most definitely deserves to be trading at a premium valuation. This certainly points to the company being undervalued.

Berkshire Hathaway recently purchased a reported 1.28 Million shares of DPZ at a price of $400-$430, showing they also believe the company is undervalued at these levels.

So is DPZ a buy?

As of January 17th 2024, DPZ seems like an amazing company at a great price. It is certainly a long term compounder and I do not think the 334% return over the last 10 years was out of the ordinary.

Although it currently suffers from substantial long-term debt, the company is more than capable of meeting its current levels of debt along with its interest payments.

Taking all this into consideration, I believe DPZ is a Buy at today’s prices, an opportunity to buy a world-class company at a fair price is not to be passed up, and I think this company’s future is bright.