Is It Time to Buy LVMH?

An In-Depth Analysis of The Luxury Goods King.

LVMH, traded under the tickers MC.PA and LVMUY, stands as the undisputed titan of the global luxury goods market. It is a sprawling empire built meticulously on desire, craftsmanship, and an unparalleled portfolio encompassing 75 prestigious Maisons, or houses, spanning six distinct sectors from high fashion and leather goods to fine wines and spirits.

For years, its growth trajectory seemed almost inexorable, a testament to the enduring appeal of its brands and the strategic acumen of its leadership. Yet, recent market turbulence, coupled with a noticeable deceleration in growth, prompts a crucial question: are cracks beginning to appear in this glittering façade? Is the king of luxury goods losing some of its lustre?

The headwinds facing LVMH are undeniable. Recent financial reports indicate slowing growth, pressure on profit margins, and increasingly fierce competition, particularly from rivals adopting different strategies. Nevertheless, the sheer power of its brands and the resilience afforded by its diversification remain formidable strengths. This article will weigh these factors, examining the group's structure, strategy, performance, valuation, and competitive positioning to determine whether the current share price represents an attractive entry point for investors or warrants a more cautious stance.

An Empire Forged in Luxury

The success of LVMH is underpinned by its unique structure, operating across six core business groups. These include Wines & Spirits, home to iconic champagne houses like Moët & Chandon and Veuve Clicquot, alongside the globally renowned Hennessy cognac; the powerhouse Fashion & Leather Goods division, featuring Louis Vuitton, Christian Dior, and Fendi; Perfumes & Cosmetics, with brands such as Dior and Guerlain; Watches & Jewelry, bolstered by recent acquisitions like Tiffany & Co. alongside stalwarts TAG Heuer and Bulgar; and Selective Retailing, dominated by the beauty giant Sephora and the travel retailer DFS.

This vast network operates through more than 6,300 stores worldwide , projecting an image of global dominance. Despite its immense scale, the group officially promotes a 'family-run' ethos, emphasizing a commitment to the long-term development and unique identity of each individual Maison.

This carefully cultivated image of long-term stewardship sits alongside the formidable reputation of its Chairman and CEO, Bernard Arnault, the architect of modern LVMH. His relentless acquisition strategy over three decades has earned him monikers such as the "Wolf in Cashmere," reflecting a sometimes ruthless pursuit of prized assets. Key milestones in this empire-building include the foundational acquisition of Christian Dior via the purchase of Boussac, the strategic move into beauty retail with Sephora, strengthening the hard luxury division with Bulgari, and the landmark, though ultimately renegotiated, $15.8 billion takeover of American jeweller Tiffany & Co.

The underlying doctrine appears consistent: identify and acquire brands with strong heritage, even if struggling, integrate them into the LVMH machine, leverage the group's scale for efficiencies in marketing, distribution, and production, and ultimately boost profitability. This apparent contradiction between the 'family-run' narrative and Arnault's aggressive tactics might reflect a strategic duality, where long-term family control enables decisive, potent market manoeuvres – a combination that has undeniably fuelled the group's extraordinary expansion.

The power of this diverse portfolio lies in its inherent resilience. Exposure across different luxury segments and a wide geographical footprint provide a buffer against downturns in specific markets or categories. This structure is further solidified by the significant ownership stake held by the Arnault family through Christian Dior SE, ensuring continuity of strategy and control.

The successful integration of disparate brands, such as Bulgari, whose revenues reportedly doubled post-acquisition , and the strategic significance attached to the Tiffany deal for bolstering the jewellery segment and US presence, underscore a core LVMH competency. This competency lies not merely in owning prestigious brands, but in actively managing this complex portfolio, extracting synergies, and enhancing the value of acquired assets – an operational expertise that forms a crucial, if less visible, competitive advantage over less diversified competitors.

Performance Under Pressure

After several years of exceptional post-Covid growth, LVMH's performance moderated significantly in 2024, reflecting a more challenging economic and geopolitical environment.

Full-year revenue reached €84.7 billion. While this represented a slight organic increase of 1 percent, it marked a 2 percent decline on a reported basis compared to 2023's €86.2 billion, largely due to substantial negative impacts from exchange rate fluctuations, particularly affecting the Fashion & Leather Goods and Wines & Spirits divisions.

Profitability also faced significant headwinds. Profit from recurring operations fell 14 percent year-on-year to €19.6 billion, down from €22.8 billion in 2023. This decline compressed the group's operating margin to 23.1 percent, a notable decrease from the 26.5 percent achieved the previous year, although still significantly above pre-pandemic levels. Despite this slowdown, Bernard Arnault highlighted the group's "strong resilience" amidst the uncertainty.

Performance varied across divisions; the Wines & Spirits group was particularly weak, suffering an 8 percent organic revenue decline and a steep 36 percent drop in profit from recurring operations, attributed to ongoing demand normalisation. The crucial Fashion & Leather Goods division fared relatively better, with organic revenue down just 1 percent, but still experienced a decline in operating profit. The significant negative currency impact underscores a vulnerability; despite global diversification offering resilience, reported results can be materially skewed by external factors like FX rates, potentially masking or exaggerating underlying operational trends for investors.

The challenging conditions persisted into the beginning of 2025. First-quarter revenue came in at €20.3 billion, representing a 2 percent reported and a 3 percent organic decline compared to the same period in 2024. These figures fell short of analyst expectations, signalling continued pressure on the luxury consumer. The slowdown appeared broad-based, impacting nearly all divisions, though some felt the chill more acutely than others. Wines & Spirits saw the sharpest organic contraction at 9 percent, reflecting ongoing weak demand for Cognac and normalisation in Champagne sales.

The critical Fashion & Leather Goods division also shrank by 5 percent organically, partly due to a tough comparison against a strong Q1 2024 in Japan. Perfumes & Cosmetics dipped 1 percent organically, while Watches & Jewelry held stable with 0 percent organic growth, and Selective Retailing also saw a slight 1 percent organic decline. The relative stability of Watches & Jewelry, compared to the more significant declines elsewhere, might hint at greater resilience in high-end hard luxury or perhaps offer an early, tentative sign of the positive contribution from the recently integrated Tiffany & Co. filtering through. Further results will be needed to confirm if this relative strength is sustainable.

The regional performance in the first quarter of 2025 painted a mixed picture. Europe managed to achieve growth on a constant currency basis. However, the important United States market registered a slight decline overall, despite some bright spots in Fashion & Leather Goods and Watches & Jewellery. Japan experienced a downturn, but this was largely anticipated given the comparison against an exceptionally strong Q1 2024, which had been significantly inflated by high spending from Chinese tourists visiting the country at that time.

The rest of Asia showed trends broadly comparable to those seen in 2024. This specific weakness in Japan highlights LVMH's sensitivity not just to local economic conditions but also to global travel patterns and the spending habits of key consumer groups, particularly Chinese nationals. Forecasting performance therefore requires analysing not only local demand but also international tourism flows and the economic health of major tourist-origin countries. These regional results reinforce broader concerns about softening demand in the key growth engines of China and the US, factors contributing to the overall deceleration.

Valuing the Luxury Behemoth

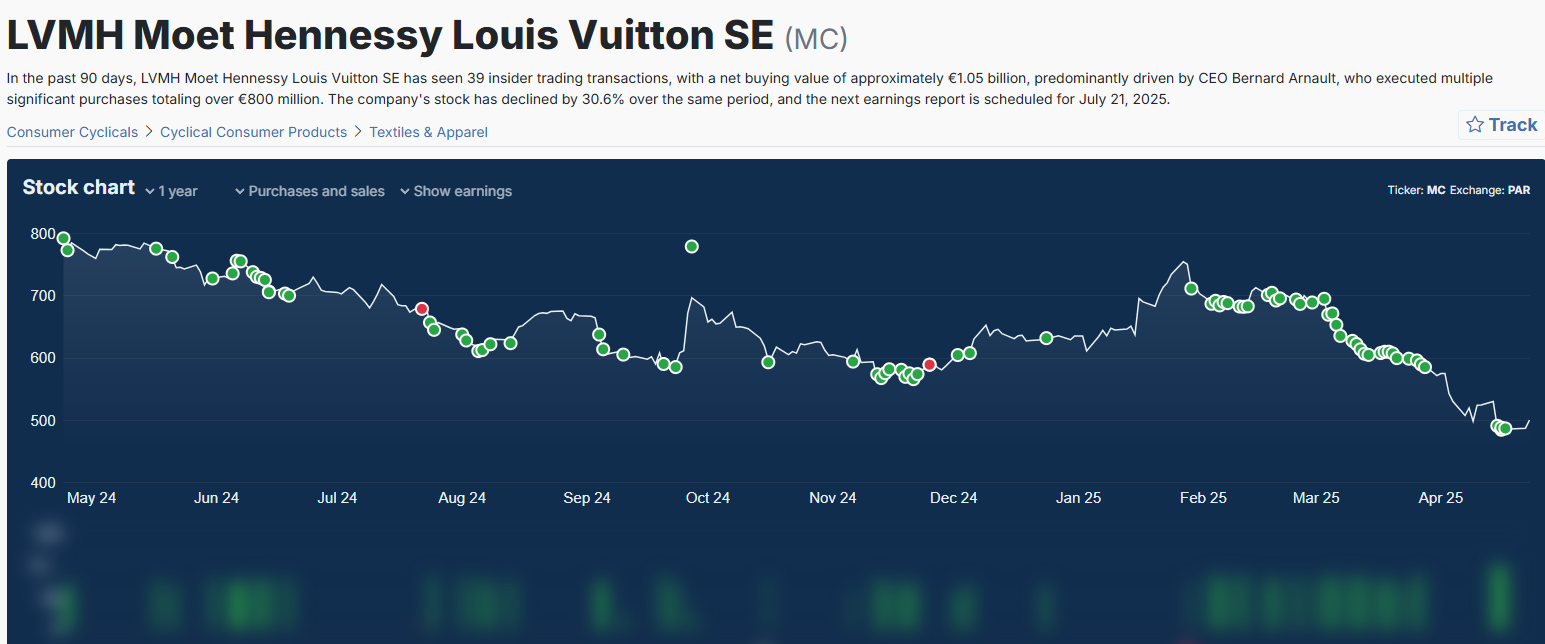

Reflecting the recent operational slowdown and broader market concerns, LVMH's share price has come under significant pressure. The Paris-listed shares (MC.PA) have recently traded near down to their 52-week low of €471.25. As of writing, the stock was trading around €500, representing a steep decline of over 37 percent over the last year. Similarly, the US-listed ADRs (LVMUY) are trading in the $111-$116 range, also significantly off their highs.

This price decline has brought valuation metrics down from potentially elevated levels. The group's market capitalisation stands at approximately €250 billion. The trailing twelve-month Price/Earnings (P/E) ratio is hovering around 19 to 20 times earnings, a level that appears reasonable compared to historical peaks, although still demanding for a company experiencing growth headwinds. The Price/Sales ratio is approximately 3x. For income investors, the dividend approved for the 2024 financial year was €13.00 per share, translating to an annual dividend yield of around 2.60% at recent prices.

Analyst perspectives offer some support at current levels. Morningstar, for instance, maintains a fair value estimate of €650 per share for MC.PA following the weak Q1 2025 results, implying the stock is trading at a considerable discount of around 25 percent to their assessment of its intrinsic worth. This valuation is underpinned by Morningstar's 'Wide Moat' rating, primarily reflecting the strength of LVMH's brands, particularly Louis Vuitton's ability to command premium pricing through tightly controlled distribution and avoidance of discounting.

However, the counterargument, also noted by Morningstar, is that the group's aggressive acquisition strategy can lead to significant capital being tied up in goodwill and intangibles, potentially dampening overall returns on invested capital.

A crucial aspect of LVMH's valuation is its comparison with key competitors, most notably Hermès International. In a striking development in mid-April 2025, Hermès briefly surpassed LVMH to become France's most valuable company by market capitalisation, despite LVMH generating vastly greater revenues (€84.7 billion vs €15.2 billion in 2024). This highlights a significant valuation differential. Hermès consistently trades at higher multiples, suggesting the market places a substantial premium on its perceived stability, extreme exclusivity derived from a single-brand focus, and potentially higher and more consistent margins.

Conversely, LVMH may suffer from a 'conglomerate discount', where the market values the sum of its diverse parts less highly than a pure-play luxury icon like Hermès, possibly due to the complexity and varying margin profiles across its portfolio (e.g., lower-margin Sephora versus high-margin Louis Vuitton). This implies that while LVMH's diversification provides operational resilience, it might come at the cost of a lower overall valuation multiple compared to the perceived purity and focus of its rival.

The Competition

LVMH operates in a highly competitive luxury market, facing off against other powerful conglomerates and strong independent brands. Its main rivals include Kering, which owns Gucci, Saint Laurent, and Bottega Veneta; Compagnie Financière Richemont, focused on hard luxury with brands like Cartier, Van Cleef & Arpels, and IWC Schaffhausen; and the unique case of Hermès, renowned for its ultra-exclusive status. Other significant players vying for the affluent consumer's wallet include the privately held Chanel, beauty giants Estée Lauder and L'Oréal in the perfumes and cosmetics space, Italian fashion houses like Prada, and British heritage brand Burberry.

The strategic contrast between LVMH and Hermès is particularly telling. LVMH pursues growth through a multi-brand conglomerate model, leveraging scale and diversification across its 75 Maisons. Hermès, by contrast, focuses intensely on cultivating the desirability of its single brand through extreme exclusivity, carefully managed scarcity (epitomised by waiting lists for its Birkin and Kelly handbags), and catering primarily to the very wealthiest clientele. This difference in approach appears to grant Hermès greater resilience during economic downturns, as its core customers are less affected by cyclical swings.

However, this strategy inherently limits Hermès's potential scale compared to LVMH's broader reach. The history between the two is also marked by Bernard Arnault's failed attempt to gain control of Hermès through a stealth accumulation of shares around 2010, a move ultimately thwarted by the Hermès family, further highlighting their divergent paths. This competitive landscape demonstrates that multiple paths to success exist in luxury: LVMH bets on breadth and integration, while Hermès prioritises depth and exclusivity.

Despite the intensifying competition and recent slowdown, LVMH retains formidable competitive advantages. Its unparalleled portfolio of diverse, iconic brands remains its greatest asset. This is complemented by its vast global scale, encompassing a distribution network of over 6,300 stores , and significant financial muscle allowing for substantial investment in marketing, innovation, and store environments. The group has a proven track record of successfully acquiring and integrating brands, turning them into more profitable entities within the LVMH structure.

It holds dominant positions in key segments, particularly Fashion & Leather Goods, which accounts for nearly half of group revenue, and Selective Retailing, driven by the strength of Sephora. LVMH also boasts significant market share in specific niches, such as an estimated 12.1% share of the US Perfume & Fragrance Store market. Furthermore, the ownership of Sephora provides a unique competitive edge – direct control over a major multi-brand retail channel, offering invaluable market intelligence and a powerful platform for its own beauty brands, an advantage most rivals lack.

However, LVMH is not without potential vulnerabilities. The aforementioned conglomerate discount suggests the market may struggle to value its diverse assets cohesively. Managing the desirability and exclusivity across 75 different Maisons presents an ongoing challenge, with the risk of brand dilution or internal cannibalisation if not handled carefully. The group's performance appears somewhat more cyclical than ultra-exclusive peers like Hermès. Finally, maintaining consistent execution, fostering innovation, and retaining key creative and managerial talent across such a vast and complex organisation remain critical operational hurdles.

Risks and Uncertainties

LVMH currently navigates a complex web of risks and uncertainties. Foremost among these are macroeconomic clouds gathering over key markets. The clear slowdown in luxury demand following the post-pandemic surge is evident in recent results. Weakening consumer sentiment in crucial regions like the United States and China, driven by inflation, higher interest rates impacting discretionary spending, and potential "spending fatigue" after years of strong consumption, poses a significant threat to future growth.

Compounding these economic worries are geopolitical tensions and the spectre of protectionism. The threat of escalating trade wars, particularly potential tariffs imposed by the US on European luxury goods, looms large and could significantly impact profitability. The convergence of this trade uncertainty with the existing macroeconomic slowdown creates a particularly challenging backdrop, as tariffs could exacerbate weak demand by forcing price increases or restricting market access. Bernard Arnault's public call for a free-trade area between the US and Europe , and his reported concerns about the European Union's stance on tariffs, suggest this is a high-priority issue at the highest levels of the company, indicating the potential material impact foreseen from such policies.

Beyond these external factors, LVMH faces company-specific challenges. Its global operations leave it significantly exposed to currency fluctuations, which can materially impact reported earnings, as seen in 2024. The ongoing task of successfully integrating major acquisitions, such as Tiffany & Co., requires careful execution to realise expected synergies and justify the purchase price. Maintaining brand desirability and the perception of exclusivity across an ever-expanding portfolio of 75 Maisons is a delicate balancing act. Ensuring consistent innovation and operational excellence across such a diverse and decentralised organisation, while retaining key talent like designers and executives, remains a perpetual management challenge.

Final Verdict: Time to Buy, Hold, or Fold on LVMH?

In weighing the investment case for LVMH, the scales present a complex balance. On one side, the strengths are undeniable: an unmatched portfolio of globally recognised and desired luxury brands, significant diversification across product categories and geographies providing resilience, a proven ability to acquire and enhance valuable assets , and substantial financial resources. The Wide Moat, reflecting brand power and pricing control, speaks to its long-term competitive advantages. On the other side, the weaknesses and risks are currently prominent: clear evidence of a growth slowdown and margin pressure in recent results, heightened vulnerability to macroeconomic downturns and geopolitical shocks like trade wars, intense competition from formidable rivals, and a valuation that may be hampered by a conglomerate discount.

The valuation question is central to the decision. LVMH shares have retreated significantly, trading near recent lows with a P/E ratio around 20 times trailing earnings. This represents a discount to some analyst fair value estimates, suggesting potential undervaluation. The critical judgment is whether this discount adequately compensates investors for the heightened risks and uncertainty surrounding near-term performance.

Ultimately, LVMH is undoubtedly facing its most significant test since the global financial crisis. The slowdown in luxury spending is real, impacting performance across most divisions, and the geopolitical climate adds a layer of unwelcome uncertainty, particularly regarding trade relations. While the allure of buying the world's premier luxury conglomerate at a discounted valuation is certainly tempting, the lack of clear visibility regarding the timing and strength of a demand rebound, especially in the crucial Chinese market, combined with a valuation that, despite the recent fall, remains relatively demanding compared to the broader market, counsels a degree of caution.

For investors with a genuinely long-term horizon and a high tolerance for volatility, initiating a small position or 'nibbling' at these levels might be justifiable, predicated on the belief in the enduring power and desirability of core brands like Louis Vuitton and Christian Dior eventually overcoming the current cyclical downturn. However, for those seeking greater certainty before committing significant capital, waiting for concrete signs of demand stabilisation and improving margins, perhaps looking for confirmation in the next one or two quarterly earnings reports, appears the more prudent course of action. LVMH remains a titan of its industry, possessing deep structural advantages. Yet, even titans can stumble under pressure. At this juncture, the investment case feels more akin to a 'Hold' than an outright 'Buy', unless one possesses an unusually strong conviction in a swift and robust recovery in the global luxury market.

A Final Note

It should be taken into consideration that the Arnault family has been buying shares of LVMH at an unprecedented rate since it started it’s recent decline. I won’t comment on these buys but as the great Peter Lynch said, "Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.”

Thank you for reading, I hope you enjoyed!! Have a great day.