Is It Time To Buy Novo Nordisk?

After a 46% Drop...

Disclaimer: This is in no way financial advice. I am not a financial advisor. Do your own research before making any final decision on investments.

Shares in the Danish leading global healthcare company Novo Nordisk (Ticker: NVO) have seen a 46% decline over the last 7 months. Is it time to buy the dip? Or is this enormous sell-off justified? Let’s take a look:

Who are Novo Nordisk?

Novo Nordisk is a Danish company which manufactures pharmaceutical products and services, specifically regarding diabetes treatment. Its main product is the drug semaglutide, used to treat diabetes under the brand names Ozempic and Rybelsus and obesity under the brand name Wegovy.

Novo Nordisk is one half of an effective duopoly over weight loss drugs, their only competitor being the American pharmaceutical giant Eli Lilly. This is an extremely lucrative industry, with the adult obesity rate in the United States being estimated to be around 40% in 2024. This has caused an explosion in the popularity of weight loss drugs, causing NVO’s revenue generated to more than double from $4.84B to $10.3B from 2020 to 2024 (an increase of 112%).

Looking at the base business model they already look like a promising investment, so why the rapid decline in share price? Let’s take a closer look at the company.

The Positives

The rapidly expanding GLP-1 market is expected to maintain double-digit CAGR over the next 10+ years (as shown below), and ageing global populations are creating immense strength in the healthcare sector as a whole. NVO is in position to take full advantage of both these tailwinds, given their dominance in the diabetes treatment market and participation in the current weight-loss duopoly.

The Diabetes and Obesity care segment is by far the largest contributor to NVO's recent financial success. This generated almost 94% of the company's total revenue during in Q3 2024. The segment is highly profitable as it boasts a roughly 50% operating margin, contributing to the rapid revenue growth the company has seen recently. NVO looks set to capitalise on this trend, holding a patent on semaglutide until 2032.

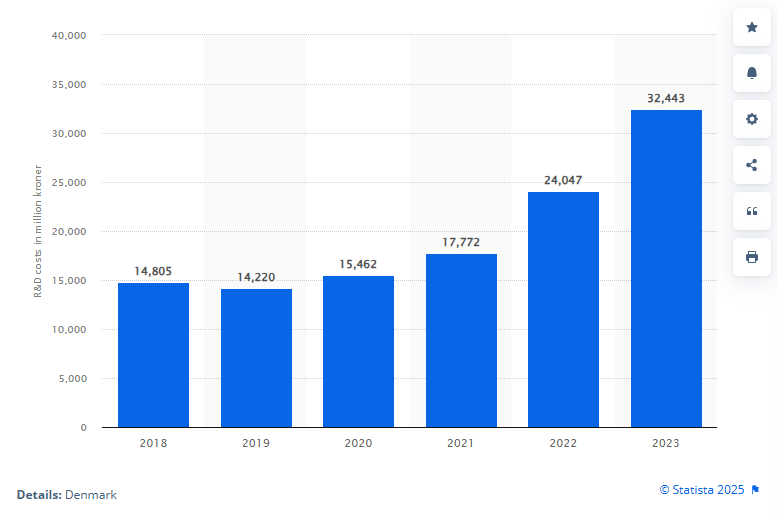

Even once this patent expires, Novo has doubled and tripled down on Research and Development spending, meaning they aren’t likely to be left behind after the patent’s expiration. With the company’s staggering nearly 85% gross margin, there is ample opportunity to reinvest in developing new products.

We have seen an average 74% ROIC over the last 10 years in Novo Nordisk, which gives me great confidence in NVO’s ability to generate more intrinsic value growth from its recent R&D spending spree.

The company currently has $11.2B in cash, and $8.5B in total debt, the balance sheet of an extremely healthy and high quality company. We can perform a DCF calculation to estimate a fair value of shares.

Using a Weighted Average Cost of Capital (WACC) of 5%, Seeking Alpha’s consensus Revenue estimate of 48B for 2025, 10% Revenue CAGR over the next 5 years, a 3% constant growth rate and Free Cash Flow (FCF) Margin of 18% we can calculate an estimated fair value of ~$128, presenting a 62.7% upside!!

This estimate of fair value combined with the strong fundamentals and flawless balance sheet makes Novo Nordisk look like the most undervalued company in the world, so why have we seen a nearly 50% decline in Market Cap in only 7 months? Let’s take a look:

The Negatives:

In 2024 Novo Nordisk acquired Catalent in a deal valued at ~$16.5 billion. The purpose of this acquisition was to sell Catalent's manufacturing facilities to Novo Nordisk in an attempt to attempt to fix supply chain problems and expand production for Ozempic and Wegovy.

The full benefits from this acquisition are not going to be realised immediately however. Management has said that that the integration of these sites is expected to have a negative impact in the low single digits on operating profit growth in both 2024 and 2025.

When a drug is on the FDA’s shortage list in the USA, compounding pharmacies can legally make copies of it. However once it's removed, compounding becomes restricted and stops within 60-90 days. Semaglutide shortages could cause this to happen, causing compounding pharmacies to increase their production of cheaper copies of the drugs to meet demand. This would be a massive hit to NVO’s quarterly earnings and is a constant risk until production ramps up.

Separately from the shortage issues, on October 22 2024 Novo Nordisk submitted an FDA request to ask that semaglutide products be added to the Demonstrable Difficulties for Compounding (DDC) list. This would prevent compounding pharmacies from making copies of Ozempic and Wegovy. The FDA has not made a decision on Novo Nordisk's DDC petition yet, and this will have to wait until after the new administration takes office under Trump. If the decision doesn't go Novo Nordisk's way, the market will most likely react negatively, creating more pain for investors.

After such a large dip, I would expect to see insiders purchasing shares at a rapid pace, however there has been zero reported buying so far, which is something I do not like to see. That being said the company did just announce a massive buyback indicating they may believe they are currently undervalued. Numerous funds did sell out of their NVO positions in the middle of last year however, and we have not seen enormous buys in this dip either, another typically negative sign for the company.

The Conclusion

Looking at other large-cap Healthcare stocks, NVO trading at a TTM P/E of 25 certainly looks cheap, especially considering their promising future growth prospects, which seem much greater than other more expensive companies.

Overall, I want to see a bottom for the company before buying in. There is currently a lot of negative momentum in the company’s share price which could certainly carry the company down from it’s current share price of $78.69 down to even $70.

Dollar Cost Averaging in looks like the most attractive option at the moment, as the company does look undervalued at current levels for a 2-5 years hold. This year there is definitely a chance of a sharp turnaround, but that currently does not look likely.