Lululemon - Stretched Too Thin

An In-Depth Analysis

For years, Lululemon Athletica (LULU) was more than just a stock; it was a market phenomenon. A purveyor of premium yoga pants that morphed into a global lifestyle brand, it came with a valuation that reflected a narrative of seemingly perpetual growth and invincibility. That narrative has now been torn to shreds. Following a disastrous second-quarter earnings announcement for fiscal year 2025, the company’s shares have been in freefall, tumbling by around 20% in the immediate aftermath and bringing the total loss for the year to more than 50%. The market darling has become a battleground stock overnight.

The central question now facing investors is whether this is a temporary, albeit severe, stumble for a best-in-class retailer, or the beginning of a fundamental unravelling of its business model. The bear case is compelling: a core US market in decline, intense competitive pressure, and a brutal, unexpected hit to profit margins from shifting trade policy. Yet, bulls point to a roaring international business, a strong balance sheet, and a management team that is now awake to the crisis. Lululemon’s success was built on selling not just apparel, but an aspirational lifestyle of wellness, community, and quality. Understanding this brand identity is crucial to grasping why the current predicament is so alarming. The threat is not merely to sales figures, but to the very essence that arguably justified its premium valuation for so long.

What the market is truly reacting to is not the marginal revenue miss reported in the second quarter, but the death of a narrative. Lululemon’s stock has historically traded at a high P/E ratio, often north of 40, a level reserved for companies whose future growth is considered almost a certainty. Such valuations are fragile, built on a foundation of consistent outperformance and a compelling story. The company’s decision to slash its full-year guidance for 2025 shattered that foundation. It was an admission that the near-term future is profoundly uncertain. This forces a complete repricing of risk. Investors who paid a premium for predictable growth are now faced with volatility and doubt, prompting a sell-off that has far outstripped the headline numbers. The market is digesting the loss of an aura, and the price action reflects that psychological shock.

Cracks in the American Dream

The source of the market’s panic can be found in the alarming deterioration of Lululemon’s home turf. The second-quarter results for fiscal 2025 laid bare a business struggling in the Americas, which still accounts for the majority of its sales. Net revenue in the region grew by a paltry 1%, but the more telling metric, comparable sales, fell by a shocking 4%. For a company that just two years ago was reporting annual revenue growth of 30% , this is not a slowdown; it is a screeching halt.

Chief Executive Officer Calvin McDonald did not mince words, admitting the company is “not happy” with its performance in the United States and identifying a critical failure in product strategy as the culprit. He conceded that product lifecycles, particularly in the casual "lounge and social" categories, have been allowed to run for too long, resulting in an assortment that has become "stale". This confession gets to the heart of Lululemon’s current paradox. The brand’s pioneering of "athleisure," the trend of wearing athletic apparel for everyday activities, was the masterstroke that propelled it into the stratosphere by vastly expanding its addressable market. However, in doing so, it transformed the competitive landscape. The primary driver for many customers shifted from pure technical performance to fashion and trendiness.

This new battlefield is Lululemon’s weakness. While legacy giants like Nike and Adidas are muscling into its core yoga and lifestyle segments, a wave of newer, more agile competitors such as Alo Yoga and Vuori are outmanoeuvring it on the fashion front. These brands are often quicker to respond to changing tastes, colours, and cuts. Lululemon, with its historically longer development cycles focused on perfecting proprietary technical fabrics like Luon and Nulu , has been caught flat-footed. The weakness in its "lounge and social" lines is proof that its technical superiority in athletic wear is no longer sufficient to dominate the very market it created. It is a victim of its own success.

A Perfect Storm for Profit Margins

As if a crisis of product and demand in its core market were not enough, Lululemon is simultaneously being battered by an external shock from US trade policy. The company’s profit outlook has been decimated by the removal of the "de minimis" exemption, a long-standing trade rule that allowed goods valued under $800 to be imported into the US duty-free. For years, Lululemon’s logistics were cleverly structured to take advantage of this provision, fulfilling a large portion of its US e-commerce orders from distribution centres in Canada. What was once a savvy cost-saving measure has transformed into a crippling liability overnight.

The financial damage is staggering. The company now expects this tariff impact to reduce its gross profit by approximately $240 million in fiscal 2025 alone. Consequently, its forecast for the full-year gross margin has been eviscerated; instead of a previously guided 110-basis-point decline, the company now expects a catastrophic 300-basis-point contraction. This has forced management into a strategic squeeze play at the worst possible time. The company is facing two distinct problems with opposing solutions. The decline in US demand due to stale products would normally call for competitive pricing or promotions to win back customers. At the same time, the massive and unavoidable cost increase from tariffs would normally demand price hikes to protect profitability.

Lululemon is therefore caught between a rock and a hard place. Raising prices to offset tariffs risks alienating an already cautious US consumer and accelerating the sales decline. Absorbing the costs, however, would mean accepting permanently lower profitability, calling into question the entire premium-brand business model. Management has indicated it will pursue a combination of vendor negotiations and "strategic pricing actions" , but this is a perilous tightrope to walk. The brand’s celebrated pricing power is about to face its most severe test in a newly hostile environment.

A Glimmer of Hope Abroad

Amid the gloom surrounding the US business, there is one powerful, undeniable bright spot: international growth. The second-quarter results presented a tale of two companies. While the Americas stagnated, the international business was firing on all cylinders. International net revenue surged by an impressive 22%, with comparable sales growing by a robust 15%. Mainland China, a key pillar of the company’s future, continued its strong performance with revenues up 25%.

These figures show that a key component of Lululemon’s long-term "Power of Three ×2" growth strategy, which aims to quadruple international revenue from 2021 levels by the end of fiscal 2026, remains firmly on track. The company is aggressively pursuing this goal, recently opening its first store in Milan, Italy, with further expansion planned for Denmark, Belgium, Turkey, and the Czech Republic. With international markets still accounting for just over 20% of total sales, the runway for growth appears extensive.

The entire bull case for the stock now rests on a "decoupling" thesis: that this international engine is powerful enough to offset the weakness in the Americas and, in time, become the primary driver of the company’s value. This thesis, however, carries a significant risk. It assumes that the problems plaguing the US market, namely brand fatigue and intensifying competition, are unique to North America. It is more likely that these are simply the challenges of a mature market. As Lululemon becomes more established in Europe and Asia, it will inevitably face the same headwinds. The moderating growth in China, down from a 30% rate in 2024 to 22% in the first quarter of 2025, may be an early indicator of this maturation process. International expansion is not a permanent cure for a core product innovation problem; rather, it is a strategy that buys the company precious time to find one.

A Strategy of Innovation and Acceleration

To its credit, Lululemon’s leadership is not in denial. Having identified a lack of "newness" as the root cause of its troubles, the company has unveiled an aggressive plan to revitalise its product assortment. The most direct action is a plan to increase the proportion of new styles from the current 23% to approximately 35% of the total offering by next spring. This represents a fundamental shift towards a faster-paced, more trend-responsive product pipeline.

Underpinning this shift is a major pivot in technology strategy, signalled by the appointment of Ranju Das to the newly created role of Chief AI & Technology Officer. The simultaneous departure of the company’s long-serving Chief Information Officer, Julie Averill, underscores the significance of this change. Das has been given a clear mandate: to leverage artificial intelligence to "expedite our product innovation process, improve our agility and speed to market, and increase personalization". This is an attempt to fundamentally re-engineer the company’s creative engine for speed.

Even amidst its struggles, the company has shown it can still innovate. The recent expansion into footwear, including the first-ever men’s collection featuring the ‘cityverse’ casual sneaker and ‘beyondfeel’ running shoe, has been a key initiative. Furthermore, the recent launch of the "Go Further" running capsule, a technical collection developed with feedback from female ultramarathoners, demonstrates that the brand’s R&D muscle has not atrophied.

However, this strategic pivot towards an AI-driven, rapid-iteration model presents a profound cultural challenge. Lululemon’s brand equity was meticulously built on a "feel-first philosophy" and the deliberate, long-cycle development of superior proprietary fabrics. The attempt to accelerate this process with technology risks a clash between a data-driven, speed-focused culture and the design-led, quality-obsessed culture that made the brand iconic. The critical question is whether Lululemon can graft the operational agility of a fast-fashion company onto the brand identity of a premium innovator without diluting the magic. The success of this corporate alchemy is far from certain.

A Coiled Spring or a Falling Knife?

The result of this turmoil has been a great "de-rating" of Lululemon’s stock. The P/E ratio has collapsed from its historical average above 40 to a TTM multiple in the low-to-mid teens, a level that would have been unthinkable just a year ago. It now trades at a discount to the broader market, a valuation more akin to a staid apparel brand than a high-growth disruptor.

The data suggests that even after its recent struggles, Lululemon maintains superior profitability metrics, particularly its return on equity. This brings the entire debate into sharp focus. The bear case is clear: the US business is broken, the product has lost its edge, and a massive tariff bill will crush margins for the foreseeable future. The stock is cheap for a reason. The bull case is equally stark: the US issues are being addressed aggressively, the international growth story is powerful and underappreciated, and the stock has been excessively punished for near-term headwinds.

The conclusion, for now, must lean towards the bear case. While the promise of international growth is alluring, the headwinds facing the company are simply too severe to ignore. The deterioration in the core US market is not a cyclical blip but a structural problem of brand fatigue and heightened competition. The tariff impact represents a direct and massive hit to profitability with no easy solution; raising prices could kill demand, while absorbing the cost guts the premium-brand model.

Management's turnaround plan, centred on accelerating innovation, is a necessary gamble but also a perilous one that could dilute the brand's quality-focused ethos. Some analysts have warned that a revenue inflection isn't expected until Spring 2026 at the earliest. The stock may look cheap on a historical basis, but it is cheap for a reason. The market is pricing in a period of profound uncertainty, and investors would be wise to heed that warning. Catching a falling knife is a dangerous game. Until there is concrete evidence that the US business has stabilised and the new product strategy is gaining traction, the risks far outweigh the potential rewards. The storm has not yet passed, and seeking shelter on the sidelines is the most prudent course of action.

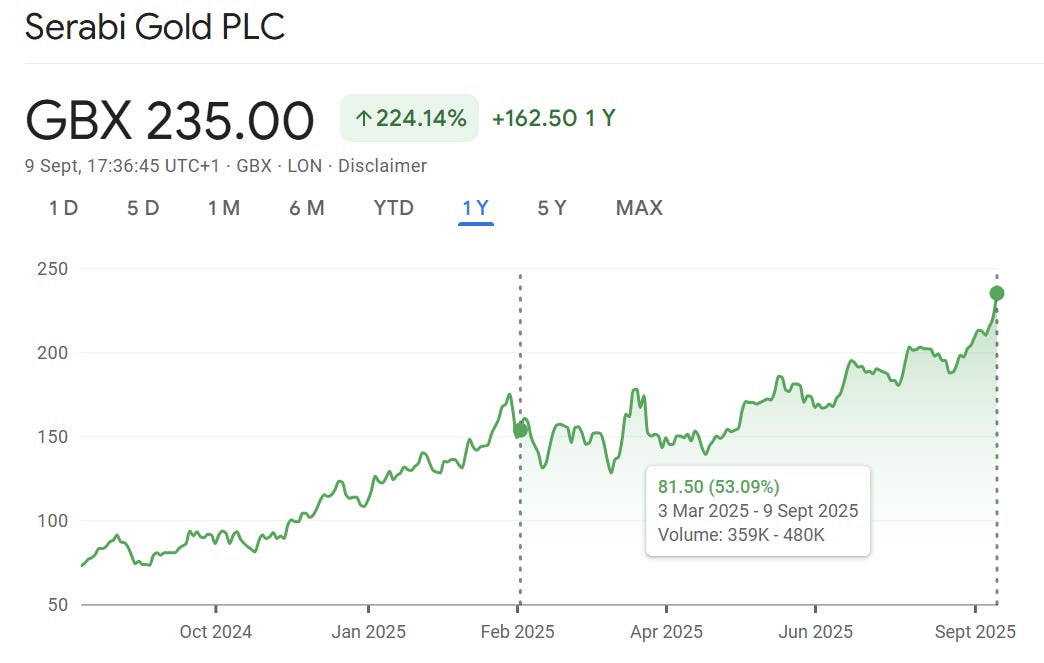

While Lululemon is interesting, it doesn't meet the stringent criteria for my Hidden Treasures portfolio, unlike Serabi Gold, which is up 53% since I added it to the portfolio 6 months ago. Paid subscribers received the deep dive on why I believe it has another 100% to run.

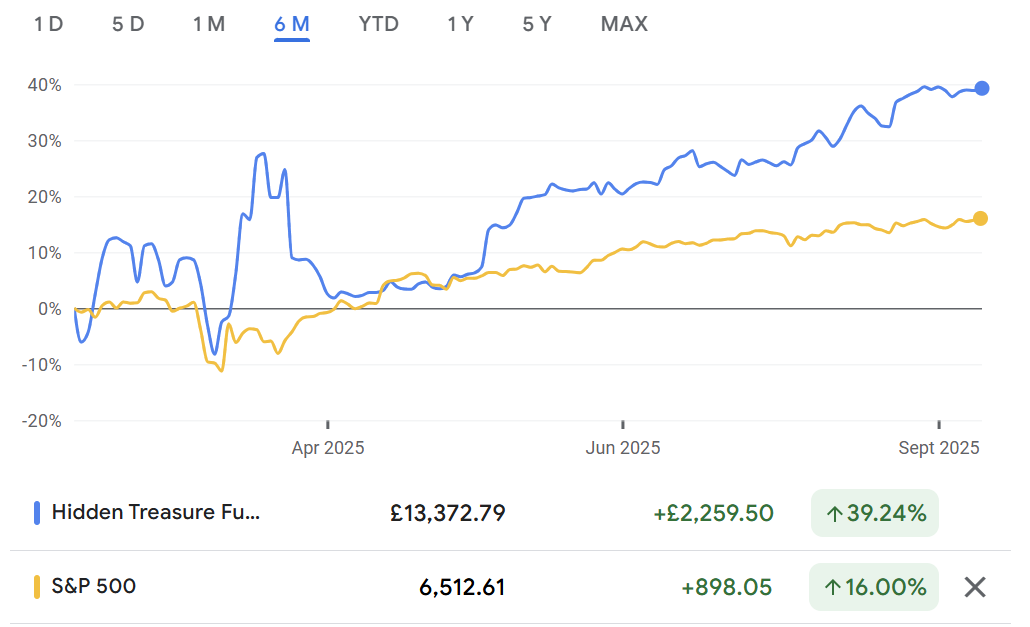

The 'Hidden Treasures' Portfolio is the engine of my paid service. Over the last 6 months, it has returned 39.2% vs the S&P 500's 16.0%. Become a paid member for access to all 11 holdings and the research behind them."

Thank you for reading, I hope you enjoyed, and have a great day!