PayPal - Complete Capitulation

Revenue is stagnant, but FCF per share is ready to double. A deep dive into the numbers behind the most hated stock in the market.

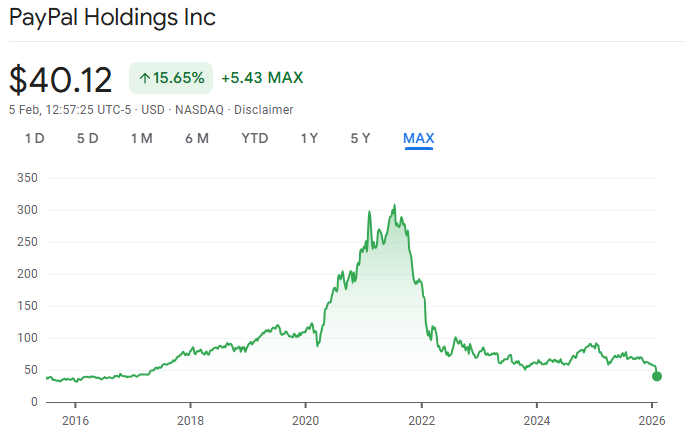

PayPal stock recently dropped 25% in 3 days, settling in the low 40s - a price level we have not seen since the company was essentially a subsidiary of eBay, long before the pandemic-induced euphoria sent it soaring to $310.

The narrative today is that it is a value trap, a dinosaur being slowly strangled by Apple Pay and at risk of being commoditised. The board has unfortunately fired CEO Alex Chriss after only 2.5 years, bringing in Enrique Lores from HP Inc.

Guidance for 2026 has been cut, and the multi-year targets that once promised a return to the glory days of 2021 have been rescinded.

What many see as the final nail in the PYPL coffin, I see as a massive dislocation between price and value.

We are looking at a business that generated over $6 billion in free cash flow in a bad year, trading at barely 7x that cash flow.

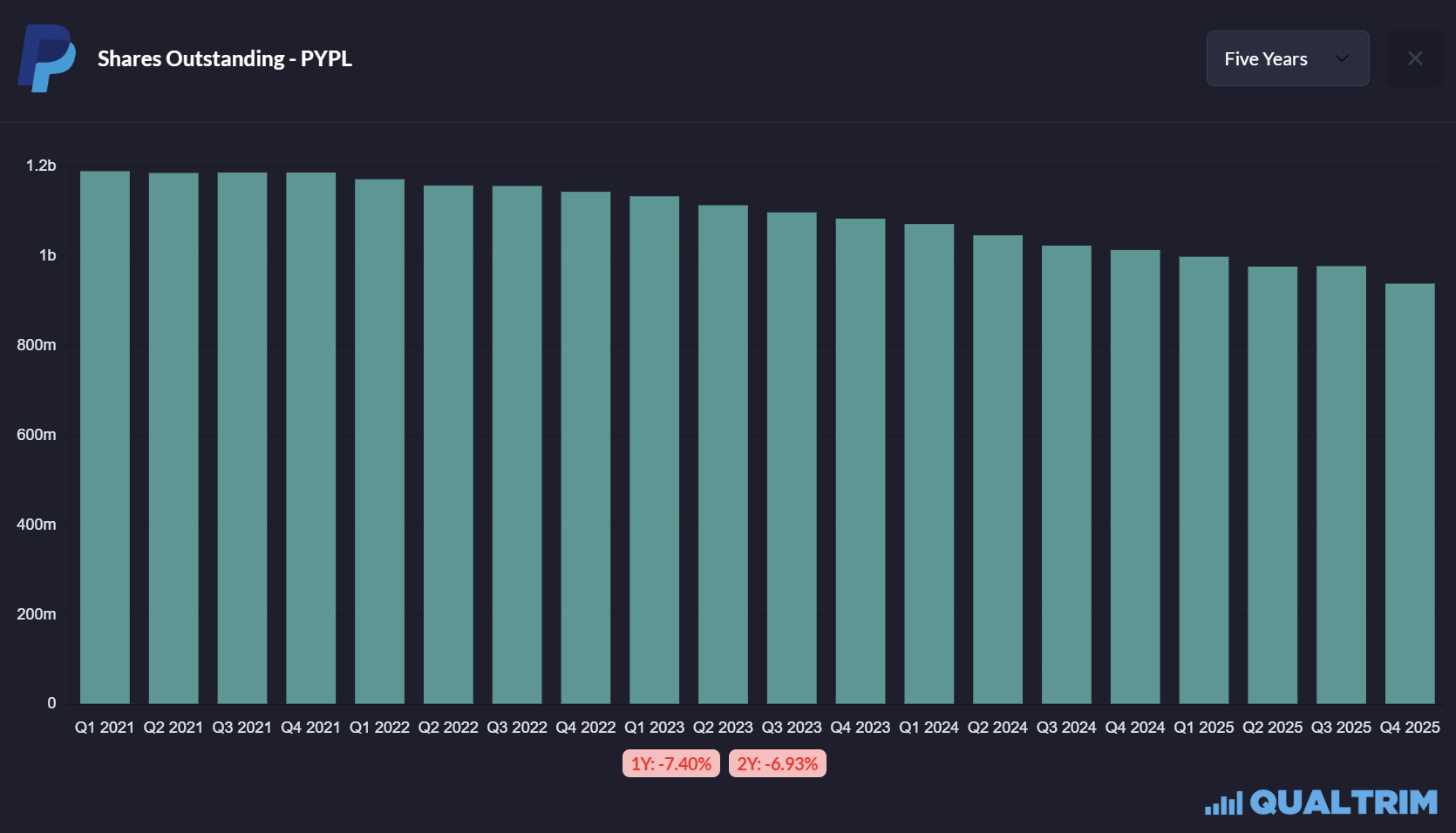

We are looking at a company that is reducing its share count at 12-15% per year.

We are looking at a balance sheet that is strong, and a turnaround that, while undeniably painful, is fundamentally misunderstood by most.

The defining characteristic of this recent sell off is capitulation. Capitulation occurs when investors surrender their previous gains or acceptance of losses in an effort to get out of the market.

It is the final stage of a bear market where the last optimistic holders finally sell. The volume on the sell-off was enormous, suggesting that institutional investors were liquidating positions regardless of price.

They were not selling because the business is worthless. They were selling because the narrative had broken.

In this report, we will review the Q4 2025 earnings objectively, stripping away the hysteria to look at the actual mechanics of the business.

We will analyse the leadership transition from Chriss to Lores and what it signals about the board’s priorities. We will explore the new advertising platform and the partnership with OpenAI that the market is currently assigning zero value.

Most importantly, we will construct a valuation model based on terrible assumptions to demonstrate that even if PayPal never grows again - even if it enters a managed decline - the stock is worth double its current price.

This article will be realistic, honest, and arguably the most important article I have written for this blog.

Q4 2025

This report was ugly.

Q4 2025 was, by most metrics, a disappointment.

Top-Line Stagnation

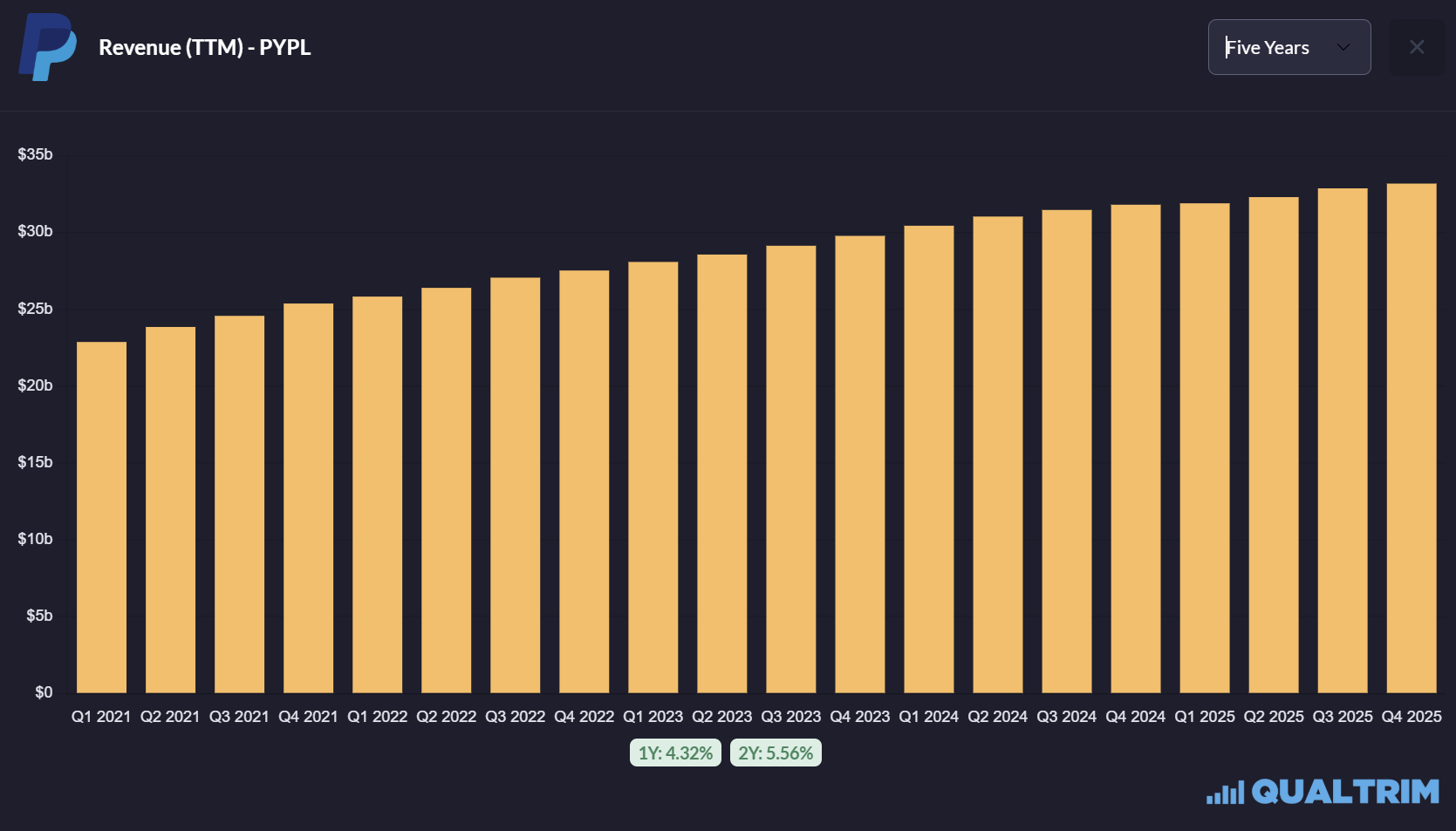

PayPal reported net revenues of $8.7 billion for the quarter, a 4% increase YoY. This missed expectations of $8.8 billion. In a market addicted to double-digit growth stories, a revenue miss of this magnitude is unforgivable.

However, let us contextualise this. We are seeing softening consumer spending across the UK, Europe, and the lower-income cohorts in the US.

The cost of living crisis is now the reality for the majority of people. For a volume-based business like PayPal, headwinds in discretionary spending are mathematically unavoidable.

The geographic composition of this revenue is telling. While US growth remains sluggish, slowed by the saturation of digital payments and Apple Pay, international markets showed resilience.

The UK and Germany, despite their own economic problems, continue to be strongholds for PayPal.

This is not a uniform collapse at all. It is a localised stagnation in the most competitive market hidden by continued utility elsewhere.

GAAP vs Reality

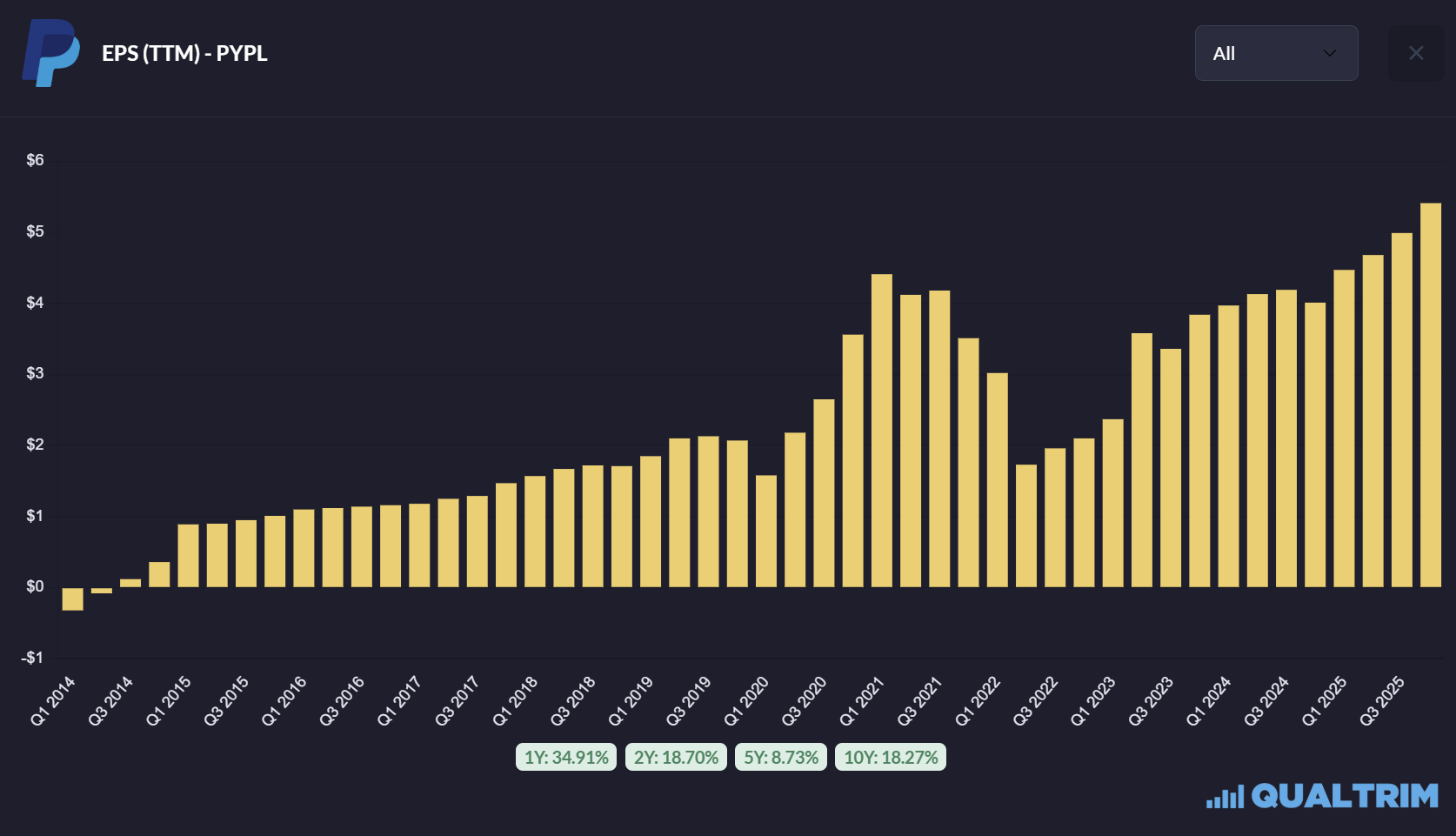

GAAP EPS grew 38% to $1.53, largely driven by favourable impacts from the company’s strategic investment portfolio - essentially accounting noise we should strip out.

The number that matters, Non-GAAP EPS, came in at $1.23, rising only 3% and missing forecasts of $1.29. When a company is priced for value, it must deliver on earnings stability. A miss here suggests that the operating leverage - one of the most important metrics for any software businesses - is not materialising as quickly as promised.

However, the reaction of the stock - dropping 20% - was not driven just by the Q4 numbers.

It was the guidance.

Management projected a ‘mid-single digit decline’ in earnings for 2026 and withdrew their 2027 targets. They guided transaction margin dollars, the gross profit of the payments business, to be ‘flat to slightly down’. For a market that values certainty, this was an invitation to sell.

Transaction Margin

The single most important metric for analysing PayPal’s health is the transaction margin dollar, which I will call ‘TM$’. This represents the revenue remaining after paying the transaction costs. It is the pure value the company extracts from its payment volume.

In Q4 2025, TM$ grew 3% to $4.0 billion. If we exclude the interest earned on customer balances - which is sensitive to interest rates and less indicative of the health of the business - the growth was 4%.

On the surface, growth is growth. But the deceleration is undeniable. The narrative that has taken hold is that unbranded processing is growing fast but at razor-thin margins, while the high-margin branded checkout, using the actual PayPal button, is losing share to Apple Pay.

The data confirms this. Branded checkout volume grew only 1% in the quarter. This is the stat that keeps investors awake at night.

If the PayPal button dies, the high-margin cash flow dies.

The fear is that Apple Pay is not just a competitor but an existential threat, removing PayPal’s moat in mobile commerce. Yet, the decline is overstated.

PayPal still commands a massive share of global e-commerce, particularly outside of the iOS ecosystem and in cross-border transactions where Apple Pay is less dominant. The 1% growth is small, yes, but it is not the negative spiral that the share price implies.

It suggests a maturity phase, a plateau, rather than a cliff.

The Unbranded Dilemma

The unbranded side of the company, primarily Braintree, continues to process enormous volumes, with TPV up 9% to $475.1 billion. However, this volume is undesirable in the eyes of the market because of the lower take rate.

The strategy under Chriss was to price-to-value - to stop competing on price alone and to bundle value-added services (risk management, foreign exchange, payouts) to expand margins.

The Q4 results suggest this transition is harder than anticipated.

Merchants are stubborn.

In a slowed economy, they fight for every tiny percentage of processing fees. PayPal’s ability to command a premium in unbranded processing is being tested by competitors like Adyen and Stripe, who are equally aggressive.

Nevertheless, we must not lose sight of the scale. PayPal processed $1.79 trillion in payments in 2025. That is roughly the GDP of Australia.

The sheer magnitude of this financial infrastructure means that even small improvements in efficiency or pricing yield hundreds of millions in cash flow.

The unbranded segment is often dismissed as a commodity business, but this ignores the massive value of the data it generates.

Every transaction processed through Braintree, even at a lower margin, feeds the data lake that powers the risk models and the ads business.

It is the top of the funnel.

Without Braintree, PayPal loses visibility into a massive chunk of global commerce. The challenge for Lores will be to monetise this visibility, perhaps not through transaction fees, but through the services that sit on top of the rails.

Interest Rates

Another factor weighing on the guidance is interest rates. PayPal generates significant revenue from the float - the interest earned on customer balances. As central banks begin to cut rates in 2026 to combat the economic slowdown, this high-margin revenue stream will shrink.

This is purely macro-driven and has nothing to do with the competitive position of the company, yet the market punishes the stock for it. I like to strip out the cyclicality of interest income to view the core earnings power.

When we do that, we see a business that is flat to slightly growing, not collapsing.

The King is Dead, Long Live the King

The most shocking development of the Q4 report was not the numbers, but the CEO change.

The announcement that Alex Chriss would step down, to be replaced by Enrique Lores on March 1st, 2026, was a shock to everyone.

Chriss had been in the seat for less than three years. He was the man brought in from Intuit to bring innovation back to PayPal. His sudden departure, framed by the board as a need for faster execution, is frankly brutal.

The Innovation Narrative

Alex Chriss promised a shock and awe innovation cycle. He spoke of profitable growth and transition years. He launched Fastlane, revamped the mobile app, and gave us the partnership with OpenAI.

These were the right strategic moves. So why is he gone?

The answer is: there is simply a gap between product announcements and P&L impact.

The board, now chaired by David Dorman, clearly lost patience with the lag time. Innovations like Fastlane are brilliant on paper - increasing checkout conversion by 50% - but their adoption curve has been too slow to offset the decay in the legacy branded business.

The execution failures cited by the board likely refers to the speed of the turnaround.

It is one thing to build a better product. It is another to get ten million merchants to install it in twelve months.

Chriss was building for a 2028 horizon. The market and the board demanded results in 2026.

Furthermore, Chriss’s tenure was marked by a communication style that often over-promised and under-delivered. The market fatigue with transition years is real. When he guided for 2026 to be another year of investment and muted growth, the board likely decided that they could not sell another year of patience to investors without some sort of a change.

Enrique Lores

Enter Enrique Lores.

This is a fascinating, if uninspired, choice.

Lores comes from HP Inc., a company that defines legacy tech. At HP, Lores was not a visionary product genius; he was an operator.

He managed a declining PC and printing business by ruthlessly cutting costs, optimising supply chains, and focusing on FCF generation. He executed workforce reductions of up to 6,000 people to save $1 billion annually.

He is a ‘wartime general’ for a mature business.

His appointment signals a shift in PayPal’s self-image. The board has essentially admitted: ‘We are not a high-growth fintech startup anymore. We are a mature financial utility, and we need to operate like one.’

Lores is not here to dream up the next Venmo. He is here to strip out the bloat. He is here to look at the operating expenses and ask why a software company needs tens of thousands of employees to maintain a code base.

For the shareholder, this is bullish. PayPal has arguably been mismanaged as a growth company for five years, spending lavishly on moonshot projects and acquisitions that destroyed value.

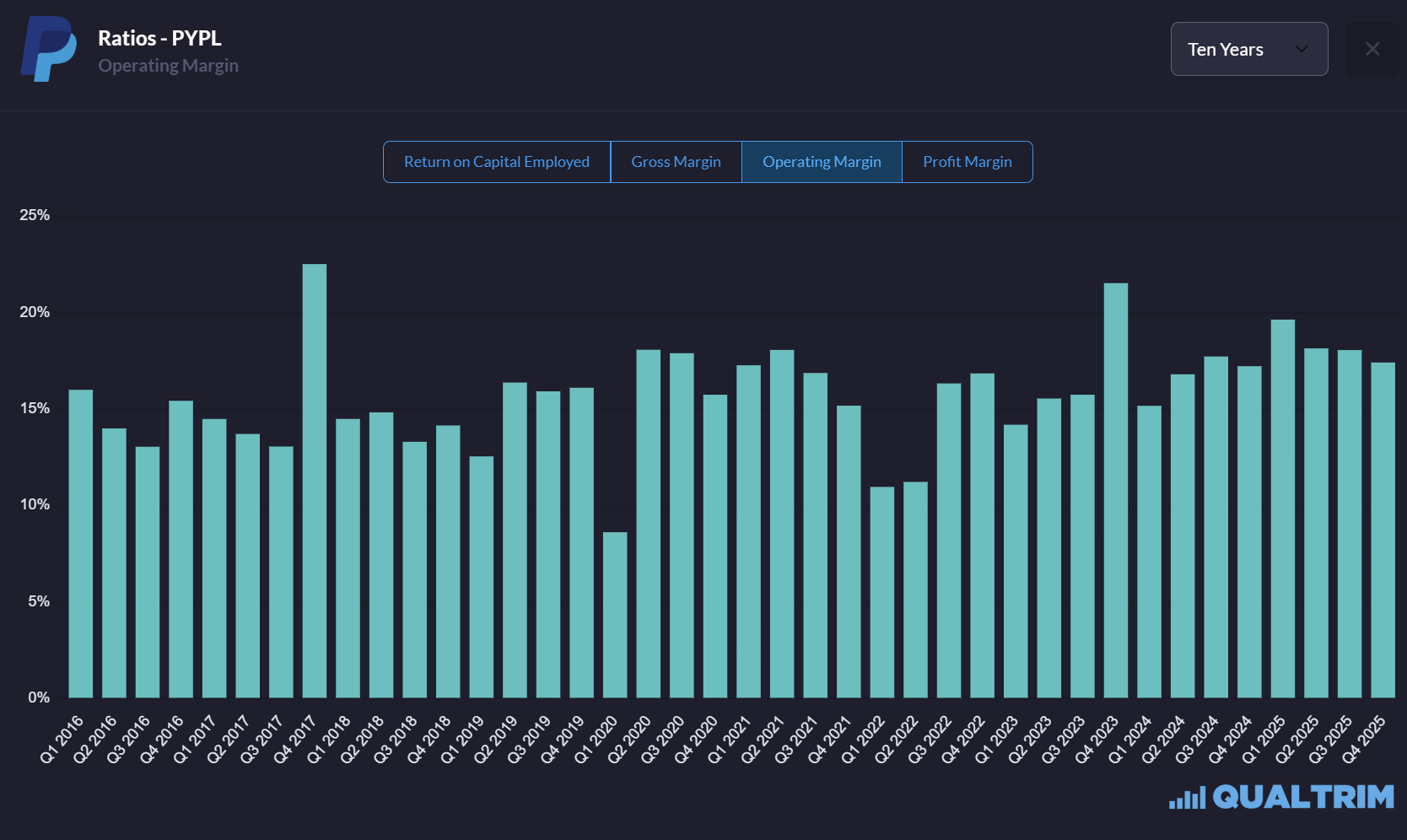

A leader who treats it like a cash-generating utility - who focuses on margins, efficiency, and capital return - is exactly what the valuation demands. Lores will likely boost efficiency and automate middle-management roles with the very AI tools PayPal is integrating, and drive the operating margin from 18% to 25% over the next three years.

He is the operator we need to protect the downside while the new products slowly gain traction.

Compensation

The details of Lores’ compensation package are instructive. He has been granted substantial equity awards, including performance stock units with a target value of $25 million.

These PSUs are linked to stock price performance over a multi-year period. This aligns his incentives directly with ours. He does not get paid the big money unless the stock price recovers.

This is not a caretaker CEO.

This is a CEO who is incentivised to engineer a re-rating of the multiple. His background in a hardware company where margins are everything suggests he will have zero tolerance for bloated R&D spend.

However, cost-cutting is only half the equation. While the market is panic-selling based on 2025 numbers, they are completely ignoring three massive drivers that are about to hit the P&L.

Below, I break down the Fastlane rollout data, the buyback mathematics, and two DCF models that prove why - even with zero growth - this stock is mathematically destined to double.