Pfizer - Beyond COVID-19

An In-Depth Analysis

Let’s be brutally honest. If you have owned shares in Pfizer over the past few years, you’ve had a terrible time. Watching a stock that was once the king of the world, the saviour of the pandemic, crumble before your eyes is a painful experience. From its peak in late 2021, the stock has collapsed by around 61%. To put that in more personal terms, a $1,000 investment made five years ago would now be worth a rather depressing $747 or so. The share price has been languishing, bouncing between a 52-week low of about $21 and a high of just over $30, a shadow of its former self.

It is easy to look at this carnage and conclude that the company is broken, that its best days are behind it. The market certainly seems to think so. The narrative is simple: the colossal, once-in-a-century revenues from the COVID-19 vaccine, Comirnaty, and the antiviral treatment, Paxlovid, were a temporary sugar rush. Now, the hangover has set in, and what’s left is a slow-growth pharmaceutical giant facing a patent cliff on its older drugs.

This is the story the market is telling itself. And in my experience, when the market becomes fixated on a single, overwhelmingly negative story, it often misses the bigger picture. The central question for us, as investors looking to beat the market, is this: Is Pfizer a classic value trap, a falling knife destined to keep falling? Or has the market’s post-pandemic pessimism created a once-in-a-decade opportunity to buy a world-class innovator at a bargain-basement price?

I believe it is emphatically the latter. The market’s punishment of Pfizer goes far beyond a simple adjustment for declining COVID revenues. It reflects a profound and, in my view, misplaced crisis of confidence in the company’s future. The stock is being priced as if innovation has ground to a halt and management is asleep at the wheel. Yet, when you look past the noise of the last two years, you see a company in the midst of a radical transformation. A company that is clearing away old uncertainties and making bold, aggressive bets on the future of medicine. The market is looking backwards, while the opportunity lies in looking at the road ahead.

The Trump Deal and the End of Uncertainty

For years, a dark cloud has hung over not just Pfizer, but the entire pharmaceutical industry: political risk. In the United States, where drug prices are the highest in the world, the threat of government intervention has been a constant source of anxiety for investors. This uncertainty reached a fever pitch under the Trump administration, with threats of crippling 100% tariffs on imported drugs and the imposition of a broad “most-favoured-nation” pricing system, which would peg US prices to the lowest levels found in other developed countries.

This kind of unquantifiable risk is poison for a company’s valuation. When investors cannot model a plausible worst-case scenario, they simply apply a massive discount to the share price. This is precisely what has been suppressing Pfizer’s stock.

Then, on 30 September 2025, everything changed. In what I view as a strategic masterstroke, Pfizer’s CEO, Albert Bourla, announced a landmark agreement with the White House. On the surface, it looked like a concession. Pfizer agreed to offer its drugs to the government’s Medicaid programme at “most-favoured-nation” prices, provide significant discounts through a new direct-to-consumer website called TrumpRx, and, crucially, commit to a massive $70 billion investment in US-based research, development, and manufacturing over the next few years.

In return for these commitments, Pfizer received the one thing it desperately needed: certainty. The deal came with a three-year grace period, a complete exemption from the threat of those punitive tariffs.

The market’s reaction was immediate and explosive. Pfizer’s stock, which had been left for dead, surged by nearly 7% on the day of the announcement and another 7% the following day, adding billions to its market capitalisation in just 48 hours. The relief was palpable, not just for Pfizer, but for the entire sector, which rallied in sympathy.

Analysts immediately recognised the deal for what it was: a clear win for Pfizer. The actual financial impact of the price cuts is expected to be minimal. The concessions are largely limited to the Medicaid programme, which accounts for a very small slice of Pfizer’s business, estimated by some to be as low as a 2% hit to EPS.

This is a textbook case of brilliant risk management. Pfizer was facing a low-probability but potentially catastrophic threat in the form of tariffs and price controls. By proactively negotiating, Bourla traded a small, known, and manageable cost for the complete removal of that existential risk. The stock’s 14% jump was not a reaction to the deal’s fine print; it was the market instantly pricing out the value of that removed uncertainty.

Furthermore, the $70 billion investment pledge was a stroke of genius from a public relations standpoint. Let’s be clear: a company of Pfizer’s scale, with an annual R&D budget of over $10 billion, was always going to be spending vast sums on research and facilities just to stay competitive. By packaging this necessary business expenditure as a patriotic concession to the administration, Pfizer generated enormous political goodwill and secured its invaluable tariff exemption, transforming a business necessity into a powerful bargaining chip. With this single move, the biggest non-financial risk hanging over the company has been neutralised. The coast is now clear for investors to focus on what truly matters: the fundamental business itself.

The Growth Engines of the New Pfizer

With the political fog lifted, we can finally analyse the company on its own merits. And what we find is not the stagnant behemoth the market seems to perceive, but a company aggressively retooling for the future, using the proceeds from its pandemic success to fund two transformative strategic pivots. Pfizer is making huge bets on what it believes will be the two most important and lucrative fields in medicine for the next decade: oncology and obesity.

A New War on Cancer

Pfizer has always been a major player in cancer treatment, but the $43 billion acquisition of Seagen, completed in 2023, was a game-changer. This was not merely about buying a few new drugs to plug revenue gaps from upcoming patent expirations on older products like Ibrance. This was the wholesale acquisition of a world-leading technology platform and a new philosophy for fighting cancer.

Seagen is the pioneer and global leader in a technology called antibody-drug conjugates, or ADCs. In simple terms, ADCs are like guided missiles for chemotherapy. They combine a highly specific antibody that seeks out cancer cells with a potent cancer-killing chemical payload. The antibody delivers the toxin directly to the tumour, killing the cancer cells while sparing healthy tissue, resulting in more effective treatments with fewer side effects. This is the cutting edge of oncology, and Albert Bourla himself has stated that the acquisition is “transforming our oncology portfolio and business”.

The deal immediately bolstered Pfizer’s pipeline, bringing four marketed products that are already generating significant revenue. The star of the show is Padcev, a treatment for bladder cancer. Its sales are growing at a blistering pace, up 38% year-over-year and on track for an annualised run rate of $2.2 billion. The pipeline is now stocked with other promising ADC candidates, such as sigvotatug vedotin for non-small cell lung cancer, giving Pfizer a clear path to growth in this critical area for years to come.

This move reveals a crucial shift in Pfizer’s strategy. The company’s management recognised that they were falling behind in the revolutionary field of ADCs. Rather than spending a decade and billions of dollars trying to build their own platform from scratch with a high probability of failure, they used the strong balance sheet, fortified by COVID revenues, to simply buy the best in the business. It was a capital-intensive move, certainly, but it was also a much faster and more certain path to securing a leadership position in the future of cancer therapy. They effectively swapped cash for time, de-risking their future revenue stream by acquiring a proven technology and a portfolio of growing, life-saving medicines.

The Weight Loss Ambition

If the move into oncology was a calculated and decisive strike from a position of strength, Pfizer’s foray into the obesity market has been a story of grit, failure, and relentless persistence. The market for weight-loss drugs is projected to be one of the largest in history, potentially reaching $100 billion by the end of the decade. For a long time, it looked as if Pfizer was going to be left on the side lines, watching rivals Eli Lilly and Novo Nordisk run away with this generation-defining prize.

Pfizer’s journey here has been fraught with setbacks. The company has had to discontinue not one, but two promising oral drug candidates. Danuglipron was scrapped due to concerns about liver safety, and more recently, in September 2025, another late-stage candidate was halted after it failed to meet its primary goals in a pivotal study. These were costly and public failures, and many investors wrote off Pfizer’s chances in the obesity space entirely.

But just when it seemed they were out of the game, Pfizer made another bold move. The company recently announced it was acquiring Metsera, a biotech firm specialising in next-generation obesity treatments, for an upfront payment of $4.9 billion, in a deal that could be worth up to $7.3 billion in total.

This acquisition is a clear signal of Pfizer’s unwavering commitment to competing in this market. Metsera’s pipeline is exciting. It includes several promising candidates, one of which demonstrated a mean weight loss of up to 14.1% in a mid-stage trial. Perhaps most importantly, some of Metsera’s injectable drugs have the potential to be administered just once a month, which would be a major competitive advantage over the current weekly injections offered by rivals.

Pfizer’s actions in the obesity market tell us something important about the company’s character. This is not a timid, bureaucratic organisation that is afraid to fail. It is an aggressive, well-capitalised company that is willing to write off its losses and immediately redeploy its resources towards a new, more promising approach. Management understands that the long-term cost of being excluded from a market as large as obesity is far greater than the short-term cost of a failed clinical trial or even a multi-billion-dollar acquisition. It is a pragmatic, if expensive, strategy that demonstrates a refusal to be shut out of one of the most significant growth areas in modern medicine.

But Is It Cheap?

An exciting story about strategic transformation is all well and good, but as investors, we know that the price you pay determines your return. This is where the investment case for Pfizer becomes truly compelling. After years of underperformance, the stock is now trading at a valuation that, in my opinion, fails to reflect the positive changes happening within the business.

By almost any metric, Pfizer looks cheap. The stock currently trades at a P/E ratio of around 14.5. To put that into perspective, the broader S&P 500 market index trades at a P/E of nearly 24. Its P/S ratio is also a modest 2.4. These are valuation multiples you would typically associate with a company in slow, terminal decline, not a pharmaceutical innovator with a pipeline of potential blockbuster drugs.

The contrast with its peers is even more stark. Eli Lilly, buoyed by the success of its obesity and diabetes drugs, trades at a P/E of over 46. The market is willing to pay a huge premium for its proven growth. Pfizer, on the other hand, is being priced for stagnation.

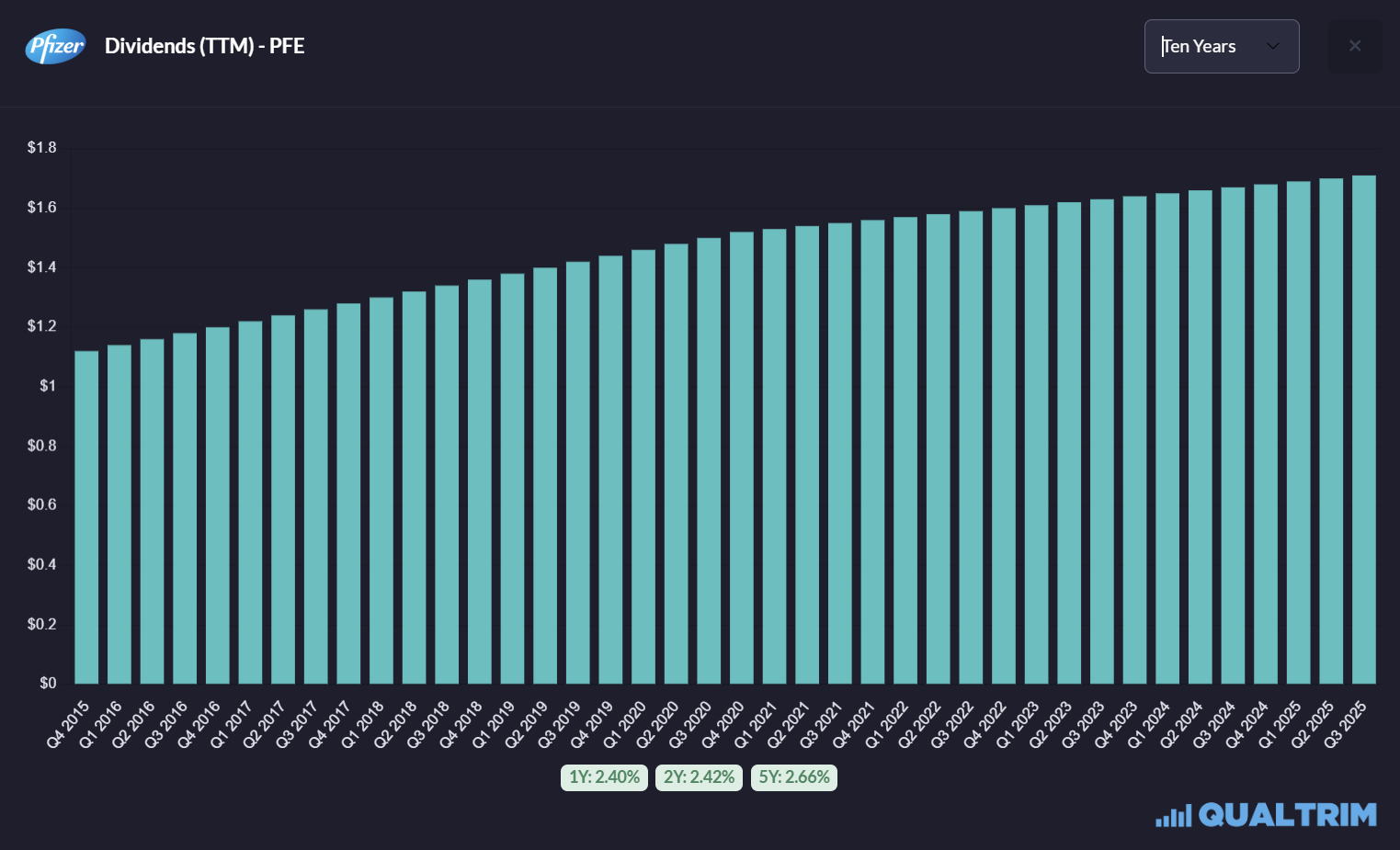

Perhaps the most attractive part of the quantitative case is the dividend. Pfizer currently offers a colossal dividend yield of around 6.3%, and has a track record of increasing that dividend for 16 consecutive years. For an income-focused investor, that is an incredibly attractive proposition.

Of course, the bears will point to the high payout ratio, which stands at nearly 90% of earnings. They argue that this is unsustainable and that a dividend cut is inevitable. This fear of a cut is a major reason why the stock is so cheap and the yield is so high. The market is pricing the dividend as a risk, not a reward.

I believe this view is short sighted. Management has repeatedly stated its commitment to the dividend, and the company’s recent performance has been strong. Pfizer beat earnings expectations in its second-quarter 2025 results and actually raised its full-year guidance for adjusted EPS to a range of $2.90 to $3.10. This provides a solid foundation to support the dividend in the near term.

Looking further out, if you believe, as I do, that the new growth engines in oncology and obesity will begin to contribute meaningfully to the top and bottom lines, then earnings will stabilise and grow. As earnings grow, that high payout ratio will naturally fall back to more comfortable levels. The market’s short-term fixation on the payout ratio is creating the opportunity. For the patient investor, the dividend is not a risk; it is a powerful source of total return. You are being paid a handsome 6.3% per year simply to wait for the market to recognise the company’s long-term growth story.

My Verdict on Pfizer

So, where does this leave us? We have a company that has been through a boom-and-bust cycle of epic proportions. A stock that has been discarded by the market, left for dead as investors chase the next hot growth story. But when we look under the bonnet, we find something very different.

We see a management team that has skilfully navigated a treacherous political landscape, removing a major source of uncertainty that was weighing on the stock. We see a company that is not sleeping idly but is making bold, transformative investments in the future of medicine, positioning itself to lead in the critical fields of cancer and obesity treatment. And most importantly for us, we see a stock that is trading at a deep discount to its intrinsic value, offering a substantial margin of safety and a huge dividend yield as compensation for our patience.

The risks, of course, are still there. The patent cliff on older drugs is real, and the company must execute flawlessly on its new pipeline. The obesity market is fiercely competitive, and success is not guaranteed. However, I believe these risks are more than adequately reflected in the current share price.

My philosophy, as regular readers will know, is that beating the market is simple, provided you know how to look past the short-term noise and identify long-term value. Pfizer, in my opinion, is a textbook example of this principle in action. The market is obsessed with the past, with the decline of the COVID franchise. The opportunity is in the future that Pfizer is spending billions to build.

For the long-term investor, I believe the combination of a de-risked political environment, a clear strategy for renewed growth, a robust balance sheet, and a deeply discounted valuation makes Pfizer one of the most compelling large-cap opportunities available today.

I believe that as the success of the Seagen and Metsera acquisitions becomes clear over the next few years, the market will be forced to re-evaluate its pessimistic stance, leading to a significant re-rating of the stock.

My verdict is a clear buy.

Thank you for reading, and have a great day!

Hi Darius, thank you very much for the in-depth analysis. Novo Nordisk is also attractively priced at the moment. How do you rate both stocks in comparison?