Stop Buying Memory Stocks

The market has confused a temporary engineering delay with a permanent physical bottleneck. The 2028 crash is already mathematically guaranteed.

Retail and institutional investors alike are currently throwing an unprecedented volume of capital into the semiconductor memory sector.

Companies including SK Hynix, Micron, and Samsung are trading at peak cycle valuations.

This flow is driven by the demand for High Bandwidth Memory, or HBM, within AI data centres.

This is, in my opinion, a mistake. What is currently happening with HBM is a temporary supply chain lag that the market is pricing as a permanent technological monopoly for companies like Micron.

These companies currently enjoy a highly lucrative bottleneck status. However, memory remains historically the most brutal, cyclical, and capital-destroying sector in the technology ecosystem.

Unlike corporations that own absolute physical bottlenecks, like GEV or ASML, the memory giants only own a temporary lead time. That lead time is mathematically guaranteed to eventually evaporate.

Below, we will examine the players in this market, the historical context of memory pricing cycles, the underlying physics of semiconductor manufacturing, and the capital expenditure war currently unfolding across Asia and the US.

We must differentiate between a hard physical limit and an industrial engineering delay.

Physical Bottlenecks

Previous analyses I published already established the concept of the true physical bottleneck. These are points in the global supply chain constrained by the laws of physics, elemental scarcity, or decades of engineering that simply cannot be replicated.

ASML operates as a true physical bottleneck (read my article on them here). The company possesses a global monopoly on EUV lithography equipment. This machinery is required to print the microscopic transistors that power every advanced logic chip globally. Consequently, ASML commands absolute pricing power and enjoys highly durable profit margins.

GE Vernova represents another true physical bottleneck (read my article on them here). The AI revolution is essentially just a new way to convert massive amounts of electricity into something useful. Data centres take electrical power and convert it into computational probability. GE Vernova manufactures the heavy electrical turbines, grid interconnects, and high-voltage transmission equipment required to physically move this energy. The company currently sits on a $163 billion equipment backlog, projected to reach $200 billion by 2027. You cannot build a heavy electrical grid in a single financial quarter. The barrier to entry is made of supply chains, regulatory permits, and unbelievably complicated engineering.

These are the companies where smart money belongs. They are immune to rapid supply shocks because the barriers to entry are absolute.

The Reality of High Bandwidth Memory

In stark contrast to lithography and power transmission HBM is constrained by an assembly learning curve.

HBM is standard dynamic random access memory. The innovation is spatial and geometric. Instead of placing memory chips flat on a circuit board, manufacturers stack the memory dies vertically.

To connect these stacked layers, engineers drill microscopic holes through the silicon wafers, fill them with copper, and then bond the layers together using thermal compression. This vertical stacking allows the memory to sit extremely close to the GPU, delivering data at incredibly high bandwidth (hence the name).

However, the current supply shortage, which has driven profits to record highs, is entirely a result of packaging difficulty. Drilling thousands of microscopic holes through silicon and aligning them perfectly is a delicate process. If a single connection in a 12-layer stack fails, the entire module must be discarded.

Because of this complexity, manufacturing yields for the latest generation of products currently hover between 50% and 60%. Standard memory chips typically see yield rates above 90%.

This 50% yield rate is the primary reason HBM is currently scarce. It is not a permanent physical limitation. It is a routine industrial engineering problem.

Samsung, SK Hynix, and Micron employ thousands of engineers. These engineers are running continuous optimisation protocols. When these engineers inevitably solve the current yield problems, the yield rates will climb from 50% to 90%

When that happens, the global supply of HBM will nearly double. This doubling of output will occur without a single new fabrication plant opening its doors. The market is pricing these stocks as if the 50% yield rate is a permanent law of nature. It is merely a temporary bridge on the path to total commoditisation.

The Graveyard

To believe that the memory sector has permanently transformed into a high-margin monopoly means ignoring 40 years of history. Memory is a commodity.

It is entirely replaceable. A memory module produced by Micron is indistinguishable from a memory module produced by SK Hynix. When products are indistinguishable, the only competitive differentiator is price.

The history of the memory industry is a graveyard. In the 1980s and 1990s, dozens of American and Japanese technology firms were forced into bankruptcy during price wars. During boom periods, memory manufacturers generate high cash flows. They take these cash flows and immediately reinvest them into larger manufacturing facilities to capture market share. Because all competitors execute this exact strategy simultaneously, a wave of new capacity eventually hits the market concurrently.

When the new capacity arrives, supply inevitably exceeds demand. Because memory factories carry immense fixed costs, manufacturers cannot afford to leave their fabrication lines idle. They cut prices to ensure their output clears the market. This triggers a race to the bottom. Margins collapse, inventory write-downs destroy balance sheets, and the sector enters a cyclical winter. This exact pattern played out in 1998, 2008, and most recently in 2018.

In 2018, the industry experienced a boom driven by the rollout of cloud computing, smart appliances, and early AI data centres. Prices rose for nine consecutive quarters. Analysts published reports declaring that the industry had finally consolidated, that pricing power was permanent, and that the boom-and-bust cycle was dead. By the end of 2019, memory prices had crashed by 33%, and corporate profits plunged by 50%.

Today, in May 2026, the exact same narrative has returned. Prominent portfolio managers are arguing that the AI supercycle has permanently altered the economics of the memory market.

The demand profile has changed, but the competitive dynamics of the suppliers have not. The memory giants are currently engaged in the largest capital expenditure war in the history of the semiconductor industry.

The 2026 CapEx War

The scale of the capacity expansion currently underway guarantees future price destruction. Across Asia, leading chipmakers have committed to spending over $136 billion in CapEx in 2026 alone, a 25% YoY increase. A significant portion of this capital is directed squarely at expanding memory production.

These companies are pouring concrete, ordering lithography tools, and building cleanrooms. The lag time between breaking ground on a new semiconductor facility and achieving full volume production is typically 18-24 months. This means the supply shock generated by these 2026 investments will hit the global market in 2028.

The executives managing these companies are trapped in a classic prisoner’s dilemma. If Samsung expands capacity and SK Hynix does not, Samsung captures total market dominance when demand rises. Therefore, SK Hynix must expand.

Because both expand, they guarantee a future supply glut. The CapEx figures are not indicators of future profitability. They are leading indicators of future price deflation.

The US has seen more investment in electronics manufacturing over the last four years than in the previous three decades combined. Planned investments are now nearly $450 billion, marking the largest wave of semiconductor manufacturing expansion in US history.

CHIPS funds have secured commitments to construct 17 new fabrication plants. This government-subsidised capacity will inevitably flow into the global supply pool, further exacerbating the oversupply.

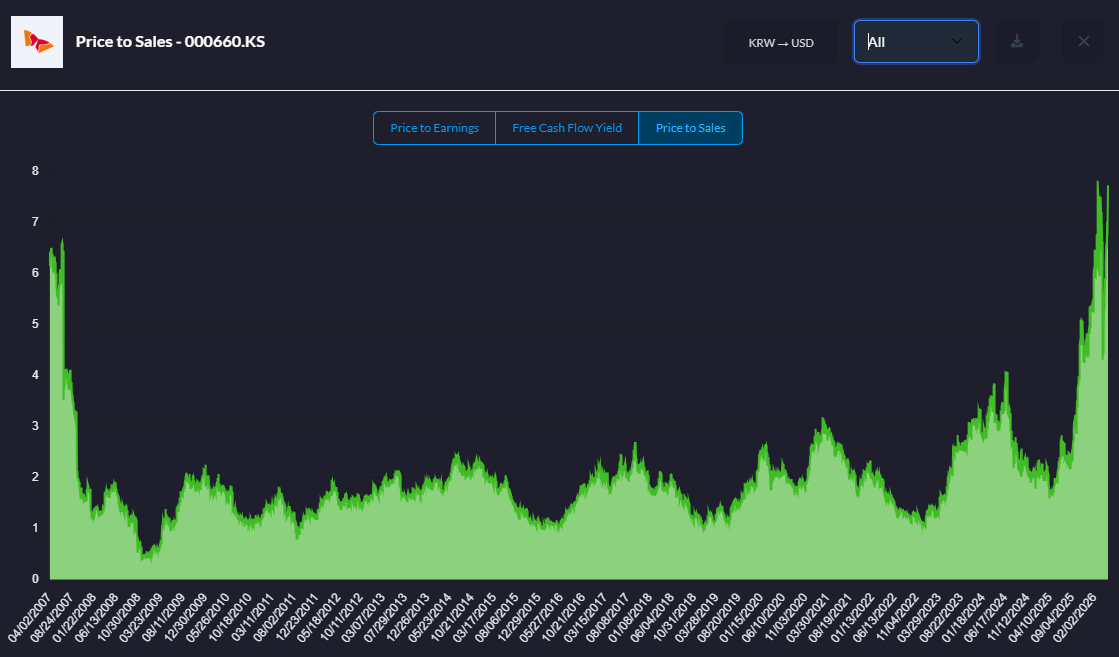

SK Hynix - The Vulnerability of the King

SK Hynix currently holds the leading position in the memory market. As of early 2026, the South Korean manufacturer owns a 62% market share in the high-performance memory sector. Their dominance is entirely tied to a first-mover advantage in packaging technology and an entrenched partnership with Nvidia.

The company recently secured ~70% of the memory supply orders for Nvidia’s next-generation Vera Rubin AI platform. This contract pushed SK Hynix’s financial metrics to record highs.

Furthermore, the company successfully upgraded its core fabrication plant in Wuxi, China, transitioning 90% of its 180,000 monthly wafer capacity to the advanced 1a nanometer process. This facility is responsible for 30%-40% of SK Hynix’s global DRAM production.

To defend its market share, SK Hynix’s board of directors recently approved an additional $15 billion capital injection into the Yongin semiconductor cluster. This specific investment brings their total commitment in the region to $21.5 billion. The funds are allocated for the construction of six advanced cleanrooms, with the company aggressively accelerating the launch timeline of the first cleanroom from May 2027 to February 2027.

While the market views these developments as positive, we must recognise the vulnerability of SK Hynix’s position. The company operates as a pure-play capacity provider at the absolute peak of a pricing cycle.

They are also highly dependent on a single major client for their highest-margin product.

If Nvidia decides to dual-source its memory components to lower its own supply chain costs, SK Hynix’s pricing power vanishes. Furthermore, by accelerating the opening of the Yongin cluster to early 2027, SK Hynix ensures their new supply hits the market exactly when competing factories come online.

SK Hynix is executing an expansion strategy that ultimately destroys its own product pricing. They are heavily exposed to cyclical downturns because they lack the diversified product portfolios of their direct competitors.

Micron Technology - The Price of Perfection

Micron Technology represents the American front in this capital war. Historically the smallest of the three major players, holding a 21%-22% market share in the advanced packaging segment.

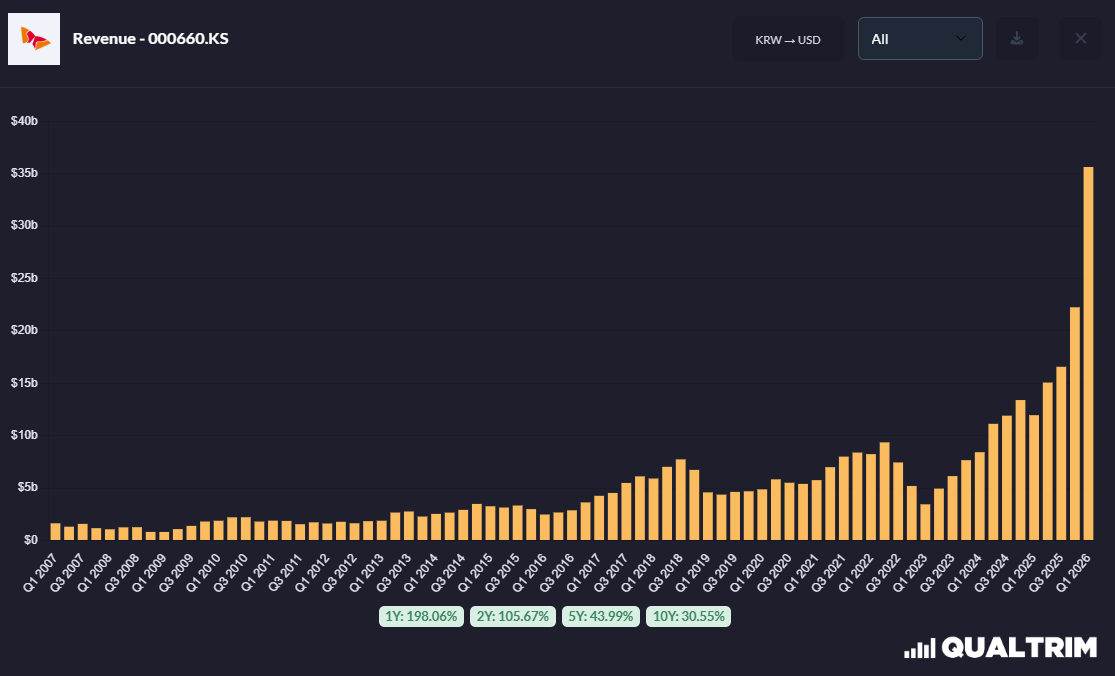

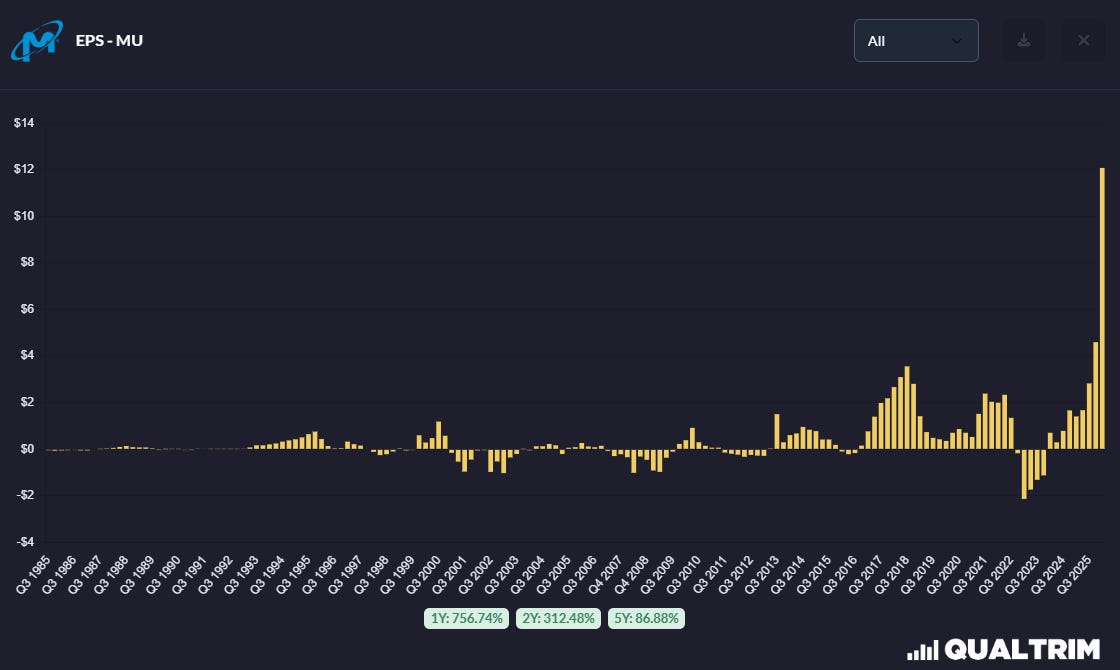

The company recently delivered a highly profitable earnings report, posting $23.86 billion in revenue and effectively tripling its performance from the previous cycle. Micron positioned itself as a technological leader, becoming the first manufacturer to mass-produce DRAM using EUV lithography at the 1-gamma node.

Management has confirmed that 100% of their advanced memory capacity for the 2026 calendar year is sold out under non-cancellable contracts.

Micron is also actively lobbying for tighter US export controls on chipmaking equipment to China to restrict competitors.

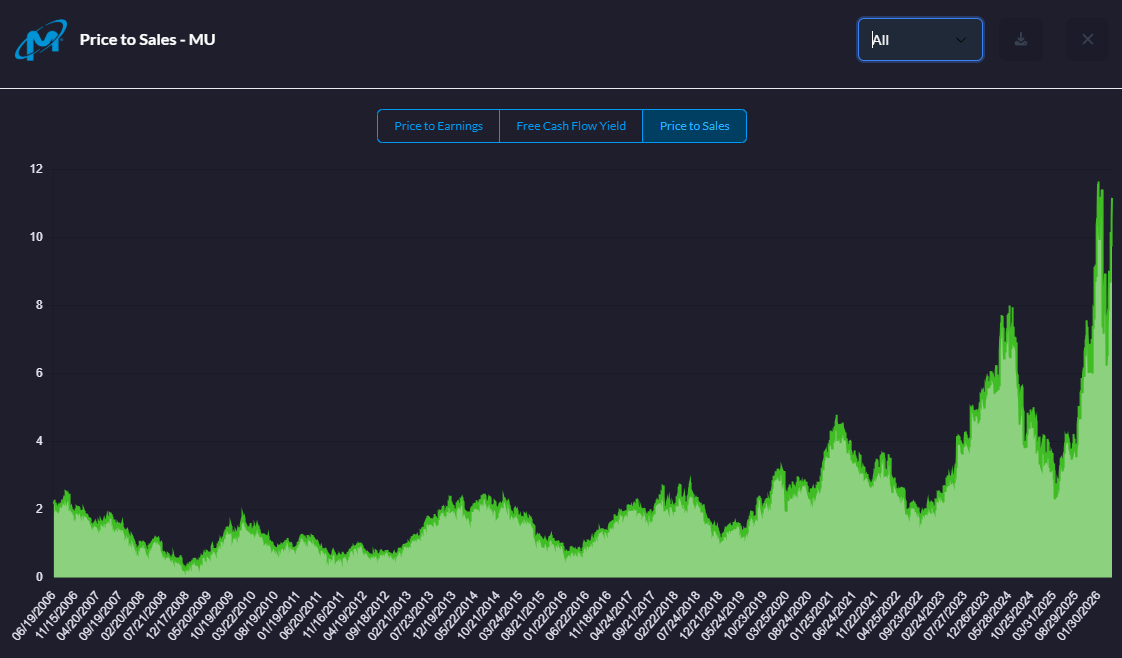

Driven by this narrative, the market has priced Micron for absolute perfection. Retail commentators frequently point to the company’s forward P/E ratio of 11x, arguing that the stock is historically cheap compared to the broader technology sector.

This valuation logic is ultimately flawed. In highly cyclical, capital-intensive industries, a low forward P/E ratio at the peak of an earnings cycle is a trap. The earnings denominator is artificially inflated by the temporary supply shortage. The market assumes Micron will maintain its current margins indefinitely. Because we are in an AI-driven period, earnings are artificially high for longer than in a normal cycle, masking the underlying risks.

Micron is planning to deploy $25 billion in CapEx this year. They are consuming vast amounts of cash to build new facilities in Boise, Hiroshima, and New York. Any macro slowdown, any delay in customer data centre buildouts, or any slight improvement in competitor yield rates will leave Micron holding billions of dollars in highly expensive, idle capacity. A perfectly run commodity business remains subject to the laws of commodity pricing.

Samsung - The Sleeping Giant

If SK Hynix is the market leader and Micron is the technological leader, Samsung is the sleeping giant preparing to flood the entire landscape.

For the past two years, Samsung found itself in an uncharacteristic position. The world’s largest overall memory producer struggled to qualify its advanced chips with Nvidia, losing significant market share to SK Hynix. Samsung’s market share in the critical advanced segment temporarily fell to 17% as they fought severe yield issues.

The company has now altered its strategy, and its response guarantees the total commoditisation of the market. Samsung committed to a staggering $73.2 billion investment in AI chip research and production facilities for 2026 alone. This single-year CapEx budget is larger than the total market cap of many global corporations. This surpasses the $50 billion CapEx set aside by TSMC for the same period.

Samsung is completely restructuring. The company slashed its memory development cycle from two years to one year. They are channeling their manufacturing capacity specifically into next-generation production, targeting mass scale for early 2026.

Samsung is now moving towards keeping the entire value chain in-house to compress competitor costs. The new 4nm process minimises power loss through low-voltage operation and low-resistance interconnects, meaning highly efficient designs.

The scale of Samsung’s intervention cannot be overstated. When a company spends $73 billion on a single hardware segment, the goal is to drown the market in volume, lower the unit cost to a level that breaks competitors, and reclaim market dominance.

Samsung anticipates its advanced memory sales will more than triple in 2026. The market views this as a bullish signal for Samsung. In reality, it is a negative indicator for the sector’s pricing power. When Samsung’s capacity successfully clears quality testing and enters the global supply chain, the current supply deficit will instantly transform into a surplus.

Supply and Demand in Data Centres

The current memory shortage is driven by the rapid scaling of hyperscaler infrastructure. Data centres will consume 70% of advanced memory chips produced in 2026. Total AI-relevant imports to the US were 111% higher in nominal dollars in early 2026 than the monthly average in 2023.

However, this demand profile is subject to strict constraints. By 2030, global data centre capacity is on course to double from 130 gigawatts to 260 gigawatts. As AI data centre networks scale, it becomes extremely important to integrate components efficiently to manage power consumption and physical space.

The ROIC for hyperscalers is THE risk. Most organisations building data centres do not expect to recoup their money in the first year. They model revenue flows over five to fifteen-year periods. If the monetisation of AI takes longer or generates lower revenues than expected, data centre projects will be cancelled or postponed. Market reactions recently diverged sharply as investors differentiated between companies where CapEx is translating into visible revenue growth and companies where expenditure is rising faster than monetisation.

If Meta, Alphabet, and Microsoft experience a deceleration in AI software revenues, they will instantly halt hardware procurement. This will travel straight down the supply chain, hitting the memory manufacturers with devastating force. Memory producers will be caught holding newly constructed fabrication plants just as their primary customers freeze purchasing orders.

The 2028 Horizon

Between the yield improvements achieved by packaging engineers and the new cleanrooms opening across the world, the physical supply of advanced memory will exponentially outpace the demand from hyperscalers. The current non-cancellable contracts will expire. As supply exceeds demand, the cost per bit will resume its historical, exponential downward trajectory.

SK Hynix, Micron, and Samsung are currently booking operating margins well above historical averages. When the price of memory plummets, these margins will compress. More importantly, the tens of billions of dollars spent on new factories in 2026 will begin flowing through the income statements as severe depreciation expenses in 2028. Declining top-line revenue combined with soaring fixed depreciation costs will obliterate net income. The forward P/E ratios that appear attractive today will explode as the earnings denominator approaches zero.

As memory prices collapse, the total bill of materials for AI servers will also drop significantly. This dynamic favours software developers, cloud providers, and end-users, but it kills the hardware supercycle. The hyperscalers will leverage the oversupply to pit Samsung against SK Hynix in contract negotiations. The value capture will migrate away from the physical component manufacturers and back toward the platform owners and power providers.

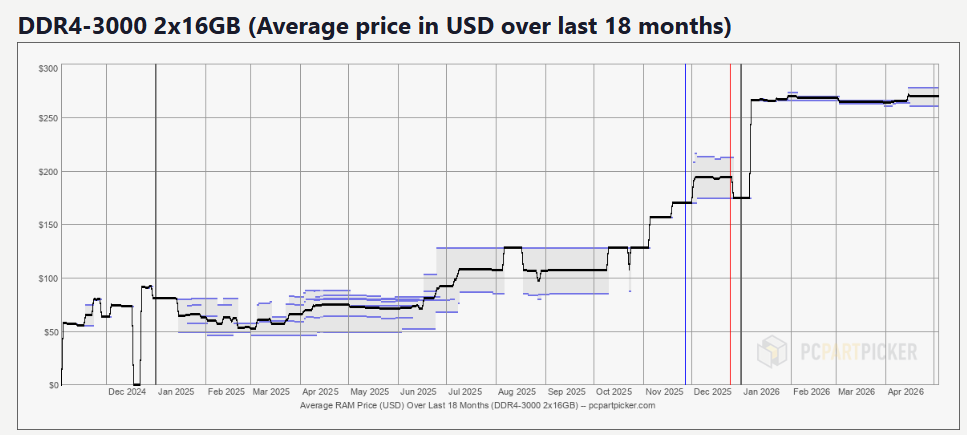

Simultaneously, the memory giants will attempt to salvage their investments by reallocating capacity to legacy consumer products. Manufacturers are currently reallocating manufacturing away from conventional DRAM to support HBM. This has artificially constrained the supply of standard consumer memory.

Consumer RAM prices have actually increased so much, it has become an internet-wide joke (which I find hilarious).

Once the advanced market cools, the factories built for high-end data centre memory will be down-shifted to produce standard chips for smartphones, laptops, and automotive applications. This capacity shift will instantly crash the price floor of the broader, traditional memory market. The entire memory sector, from the most advanced server components to the cheapest consumer storage, will enter a deflationary spiral.

Capital Allocation Strategy

Markets, as they do at the peak of any cycle, are operating in a state of mass euphoria. Participants have convinced themselves that the laws of supply and demand have been permanently suspended by AI. They are buying shares in memory fabrication companies after a multi-year run-up, relying entirely on the greater fool theory to secure an ROI.

The intelligent move today is to completely avoid allocating fresh capital to the HBM sector. The risk-to-reward ratio is broken. You are buying commodity producers at peak cyclical margins exactly as they deploy over $136 billion to destroy their own pricing power.

Capital must seek out the true physical bottlenecks of the current industrial revolution. Remain allocated in the hard infrastructure that cannot be solved by simply pouring concrete for a new cleanroom.

Leave the memory sector to the retail tourists. The fabrication plants are being built, the supply is coming, and the cycle remains undefeated.

Thank you for reading, let me know what you think, and have a great day!

Hello, my two cents - it would have been better if your article shows some concrete quantitative analysis on the projections in 2028 onwards taking into account legacy demand, AI demand, and additional supply, split by the three main products (dram, hbm, nand) and the key assumptions. There are a lot of debates between the “memory is cyclical” and “this time is different” due to change of the role of compute. However I have yet to see someone publish an in depth scenario analysis, and what I see mostly are more general convictions.

You speak as if it's so easy to improve yields from 50% to 90% 😂 and no, HBM is not indistinguishable from each other and there's a lot of work on custom HBMs being designed with certain clients