The Great Software Depression

The market believes AI is an extinction event for Salesforce and Adobe. The data proves it’s the buying opportunity of the decade.

The market is a mechanism for transferring wealth from the impatient to the patient, but in early 2026, it has become a mechanism for transferring wealth from the hysterical to the calm.

If you have listened to all the noise around software over the last four weeks, you would think the software industry is dying. The narrative is simple:

AI has mastered code generation, and therefore the marginal cost of software is trending to zero.

If a teenager in a basement can vibe code an enterprise resource planning system with a series of natural language prompts, then the moats surrounding Salesforce, Intuit, and Adobe have evaporated. The market has concluded that these giants are the next Kodak, clinging to a business model - seat-based licensing - that is destined to be left behind as ancient history.

I disagree. In fact, I view this as the greatest capital dislocation since the interest rate panic of 2022.

The market is currently pricing these high-quality compounders as if their growth will slow to zero, ignoring the reality that AI is not an extinction event for these companies but an efficiency lever of unprecedented magnitude.

While the herd panics about the commoditisation of code, they ignore the stickiness of data, the necessity of compliance, and the immense distribution power these companies have.

This is not the end of software. It is the transition from software as a tool to software as an agent. The winners in this transition will be the companies that own the workflow and the data, not the models.

There is significant fear around Salesforce, Intuit, and Adobe. I say buy the fear. Buy the panic.

In this article, we will explain exactly why the market is wrong, supported by the cold, hard cash flows and the reality of enterprise technology. If you are looking for momentum, look elsewhere. If you are looking for value in a market that has lost its mind, read on.

The Great Software Depression

The sell-off that began in January 2026 is distinct from previous corrections. It is not driven by interest rates, which have stabilised, nor by a recession, which has yet to happen. It is driven by an existential narrative.

Investors have looked at the capabilities of the latest LLMs and extrapolated a future where software is worthless because the barrier to entry - writing code - has collapsed.

This view fails to appreciate the complexity of the modern enterprise.

A big bank does not use Salesforce simply because it has the best code. It uses Salesforce because that is where twenty years of customer interactions reside, where the governance protocols are enforced, and where the security compliance is audited.

Moving off such a system is not a technical challenge of rewriting code. It is an organisational transplant of immense risk. The cost of switching is not the software license; it is the operational disruption.

Furthermore, the deflation argument ignores Jevons paradox as it applies to technology.

As the cost of software production falls, the demand for software does not stagnate.

It explodes.

Big tech is not standing still, waiting to be disrupted. They are aggressively integrating these very same AI capabilities to reduce their own engineering costs and, more importantly, to shift their business models from charging for access to charging for outcomes.

The panic has created a valuation disconnect. High-quality software names have slipped into bear market territory, with $IGV seeing one of its fastest drawdowns since the global financial crisis. This has left behind businesses trading at valuations that imply no future growth, despite guidance and contracts suggesting otherwise. Today I will focus on three specific names where the disconnect between the narrative and the reality is largest.

Salesforce

Salesforce is currently trading around $210, having been dragged down by the broader sector sell-off despite posting numbers that, in a rational market, would have sent shares soaring. The market sees Salesforce as a legacy database company, a system of record that will be bypassed by AI agents. The reality is that Salesforce is building the very platform on which those agents live.

Agentforce

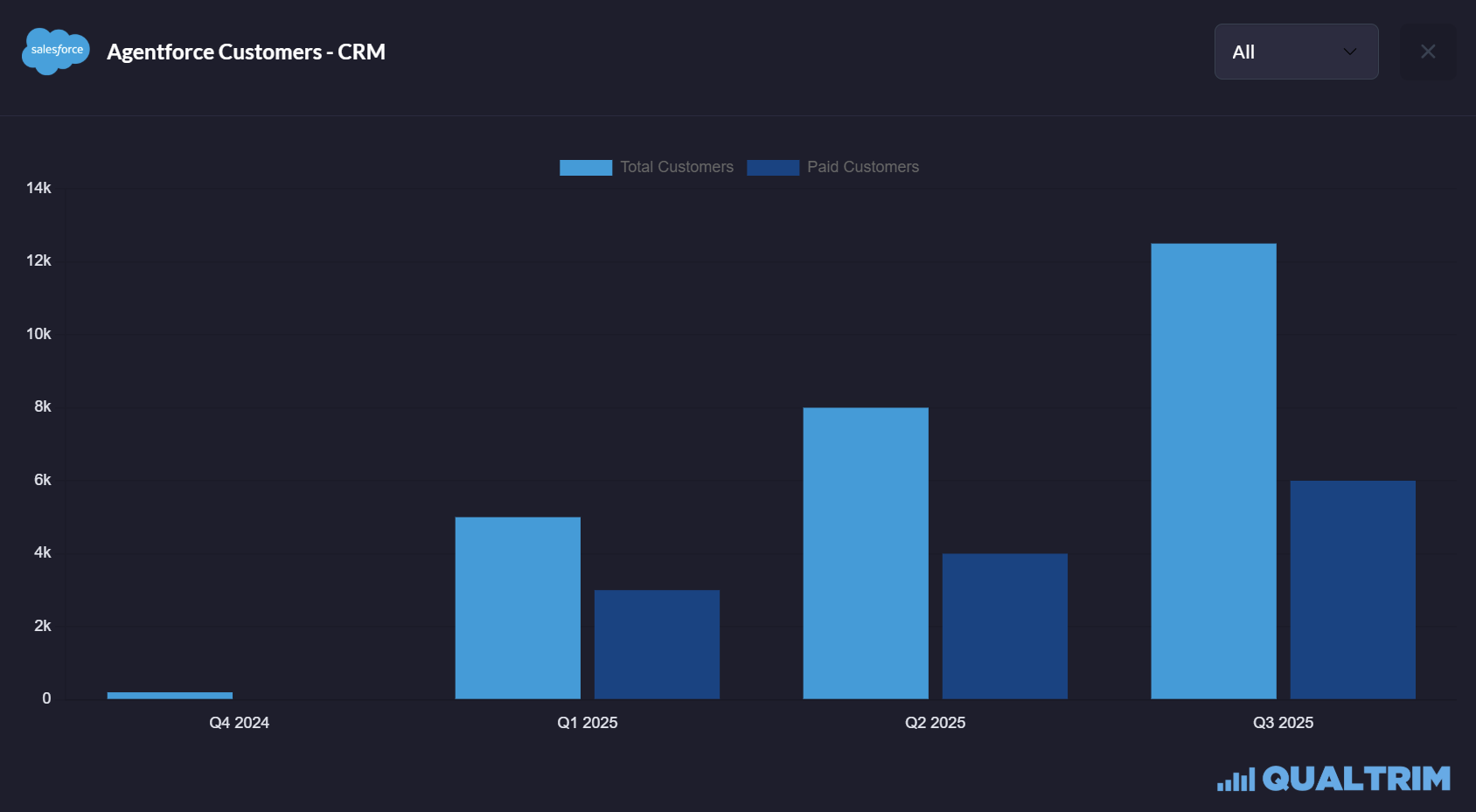

The bull case for Salesforce rests on its pivot into ‘Agentic Enterprise’. In late 2025, the company launched Agentforce 2.0, a platform designed to allow companies to deploy autonomous AI agents. The bears dismissed this as marketing fluff. The numbers prove them wrong.

In Q3 FY2026, Salesforce reported Agentforce sales of $2.3 billion, representing an 8% increase in constant currency. More significantly, the ARR for Agentforce and the Data Cloud combined reached nearly $1.4 billion, growing at a staggering 114% YoY. This is the growth profile of a hyper-growth startup nestled within a cash-generating giant.

The bearish narrative suggests that AI agents will replace the human sales reps that Salesforce monetises via seat licenses.

This is a fundamental misunderstanding of their new pricing model.

Salesforce is transitioning to consumption-based pricing for its agents. As of Q3, they had closed over 9,500 paid Agentforce deals, a 50% increase QoQ, with these agents processing over 3.2 trillion tokens.

Consider the economics.

A human sales development representative might cost an enterprise $80,000 a year. Salesforce captures perhaps $2,000 of that in software fees. An AI SDR powered by Agentforce might cost the enterprise $20,000 per annum in consumption fees. The enterprise saves $60,000, while Salesforce increases its revenue capture from $2,000 to $20,000.

This is the paradox of value in the AI era - the vendor captures a larger slice of a shrinking total cost of ownership.

The Validation

On Jan 26th, The US Army awarded Salesforce a $5.6 billion, 10-year indefinite delivery, indefinite quantity contract. This is one of the largest software contracts in federal history.

The significance of this deal cannot be overstated.

The US Army, an organisation for whom data security and reliability are literally matters of life and death, did not choose a vibe coding startup.

They chose Salesforce.

The contract covers the deployment of Missionforce, a suite of tools designed to modernise recruitment, personnel management, and operational readiness using the very Agentforce technology the market doubts.

This deal validates the strategy. You cannot have effective AI without unified data. By securing the Army’s data backbone, Salesforce has locked in a decade of revenue that is virtually immune to economic cycles.

Government contracts of this size create pull. Once an agency as large as the Army adopts a standard, the rest of the DoD and allied agencies often follow. This is a moat that no amount of vibe coding can cross.

The market is ignoring the math. Below, I break down the specific valuation models for Salesforce, Intuit, and Adobe, proving why we are looking at 40%+ upside from current levels. Let’s look at the cash flows.